Credit Risk Careers for CAs & FRMs at a Glance

If you are a CA (Chartered Accountant) or an FRM (Financial Risk Manager) candidate, credit risk is one of the easiest domains to move into right now. Indian banks must build expected-credit-loss models before a regulatory deadline, and both qualifications hand you a real head start — just different halves of the picture.

RBI (Reserve Bank of India) issued its final expected-credit-loss (ECL) directions on 27 April 2026, effective 1 April 2027, with the balance-sheet impact phased in through FY 2030–31. Banks are still on the old "incurred loss" method today — they recognise a loss only after it happens. That gap between today's rules and 2027's rules is exactly why hiring is picking up: every covered bank needs people who can build these models before the clock runs out.

It is not a distress story either. Gross NPAs (non-performing assets — loans banks have stopped earning interest on) touched a multi-decadal low of 1.8% in March 2026, per RBI's Financial Stability Report released 30 June 2026. Clean books plus a new rulebook is exactly when banks staff up on measurement, not shrink it.

What CAs bring: accounting depth in Ind AS 109 (India's version of the global IFRS 9 standard), audit rigour, and comfort with provisioning numbers. What FRM candidates bring: a full syllabus module on credit risk measurement, worth 20% of the FRM Part II exam, plus a globally recognised credential.

Credit risk analysts in India earn roughly ₹12.7–14 lakh per year in the typical experience band. That figure comes from AmbitionBox (1.8k salaries, updated 2 July 2026); we unpack the full range by experience and employer in our credit risk analyst salary guide.

Why Is Credit Risk Hiring Growing in India Right Now?

Credit risk hiring is growing because of one hard deadline and one hiring-friendly backdrop. RBI's ECL directions force every large bank to build new models before 1 April 2027. And India's unusually clean loan books mean banks are staffing this up from a position of strength, not panic.

Start with the deadline itself. On 27 April 2026, RBI notified final directions moving commercial banks — banking companies other than small finance banks, payments banks and local area banks — to expected-credit-loss provisioning. This is the biggest change to Indian bank provisioning in decades.

Two dates matter for anyone job-hunting:

| Date | What happens |

|---|---|

| 27 April 2026 | RBI's ECL directions become final (not a draft anymore) |

| 1 April 2027 | Banks must run the new three-stage ECL framework live |

| Through FY 2030–31 | The profit-and-capital impact is allowed to phase in gradually |

Plain-language takeaway: banks have about 21 months from the final rules to go live — and models, teams and documentation all have to be ready before that date, not after.

Here is the part most outsiders miss: banks are not already running ECL. They currently use the older "incurred loss" method, where a loss is booked only once there is clear evidence of trouble.

Larger NBFCs (non-banking financial companies) are the exception — the bigger ones have followed ECL-style accounting under Ind AS 109 since FY 2018–19. Banks are the ones racing to catch up, and that race is the hiring story.

The backdrop makes the case stronger, not weaker. Gross NPAs (the percentage of loans a bank has stopped earning interest on) hit a multi-decadal low of 1.8% in March 2026. That is according to RBI's Financial Stability Report, released on 30 June 2026.

Clean books do not mean risk teams shrink. They mean the discipline that produced clean books, plus a demanding new rulebook, both need more skilled people — not fewer.

Add global capability centres (GCCs — offshore teams that global banks run out of Indian cities) to the mix. The Risk Management Association of India counts more than 1,500 GCCs across Bengaluru, Hyderabad, Pune, Mumbai and Chennai.

Research firm Taggd's Decoding Jobs 2026 report finds BFSI (banking, financial services and insurance) GCCs are only about 10% of GCCs by count. Yet they employ 33% of India's GCC workforce — a heavily risk-and-compliance-staffed slice of the GCC world.

What Roles Can You Target?

Credit risk has a clear career ladder, and CAs and FRMs typically enter at different rungs. Each role answers a different question — from "should we approve this loan" to "is our own model correct." You can move up the ladder as you build experience.

| Role | What the role actually does |

|---|---|

| Credit Analyst | Assesses individual borrowers or companies before a loan is sanctioned — checks financials, credit history and repayment capacity. |

| Credit Risk Modeler | Builds the statistical models — PD, LGD, EAD (explained below) — that score borrowers and feed into ECL provisioning. |

| Model Validator | An independent reviewer who checks other teams' models for errors, bias and regulatory compliance before they go live. |

| Risk Manager | Owns a portfolio's risk exposure — sets limits, monitors early-warning signals, and reports to senior management. |

| Head of Credit Risk | Leads the entire credit risk function — strategy, model governance, regulatory liaison and team leadership. |

Plain-language takeaway: you do not need to start at the top. Credit analyst and junior modeler roles are realistic entry points for both CAs and FRM candidates; validator and manager roles come with a few years of hands-on experience.

Where you enter often depends on which qualification you hold. CAs with audit or provisioning experience frequently move straight into modeler or validator-adjacent roles. That is because so much of ECL work is documentation and reconciliation — skills a CA articleship already builds.

FRM candidates often start as credit analysts or junior modelers instead. They use the certification to signal risk-specific intent to recruiters.

Employer type matters too. Banks and large NBFCs need the full ladder in-house. Big 4 firms hire for ECL implementation projects and model validation for lender clients — work that leans on audit-style rigour as much as modeling skill.

GCCs run scorecards, stress tests and validation for parent banks abroad.

The demand is visible in live listings. On 5 July 2026, Indeed India listings for credit-risk and model-validation roles named employers such as JPMorganChase, Goldman Sachs, UBS, Citi and Nomura. Other named employers included Standard Chartered, DBS Bank, SMBC, KPMG, TCS, Genpact, Tata Capital and Aditya Birla Group.

These roles spanned Mumbai, Bengaluru, Hyderabad, Delhi and Chennai.

On pay, AmbitionBox estimates credit risk analysts earn ₹12.7–14 lakh per year in the typical experience band (1.8k salaries, updated 2 July 2026). Glassdoor puts average total pay near ₹12.25 lakh (452 salaries, July 2026). Our credit risk analyst salary in India guide breaks this down further by experience, employer type and skill.

What Does a CA Already Bring?

A CA already understands the accounting language that credit risk speaks. That includes Ind AS 109 (India's version of the global IFRS 9 standard), provisioning mechanics, and the discipline of a documented audit trail. It is a genuine head start, even though credit risk modeling itself is a new domain to learn.

Ind AS 109 is India's converged standard for financial instruments, notified under the Companies (Indian Accounting Standards) Rules, 2015. It is the accounting cousin of what RBI's ECL directions now require of banks. A CA who has worked with Ind AS 109 provisioning is not starting from zero — they already speak the standard's language.

Three specific CA strengths map directly onto credit risk work:

- Financial-statement depth. Reading a borrower's balance sheet, cash flow and ratios for red flags is core CA training — and it is exactly what feeds a credit risk model's inputs.

- Provisioning and audit experience. ECL is simultaneously an accounting number and a regulatory number. RBI's directions require documented assumptions and board-level oversight of the ECL framework — work that sits close to audit and financial-reporting skills a CA already has.

- Comfort with documentation. RBI's directions state that the criteria used to judge a "significant increase in credit risk" must be duly documented. Model documentation of this kind is second nature to anyone trained in audit working papers.

This is why CAs map naturally onto ECL implementation, provisioning and audit-facing model work. Big 4 practices are the clearest example — ECL projects for bank and NBFC clients are already live work there, not future work. If credit risk is one option among several you are weighing, our what to do after CA guide covers the wider set of post-qualification paths.

What Does an FRM Bring?

An FRM (Financial Risk Manager) candidate brings something a CA's syllabus does not. That is an entire exam section built around credit risk measurement, plus a certification that risk teams worldwide recognise on sight. It is the strongest qualification signal for a risk-specific role.

The FRM is a two-part exam. Part I is a 100-question multiple-choice exam covering risk-measurement foundations. Part II is an 80-question multiple-choice exam split across six topic areas, and one of them is built for exactly this career move:

| FRM Part II topic area | Weight |

|---|---|

| Market Risk Measurement and Management | 20% |

| Credit Risk Measurement and Management | 20% |

| Operational Risk and Resilience | 20% |

| Liquidity and Treasury Risk Measurement and Management | 15% |

| Risk Management and Investment Management | 15% |

| Current Issues in Financial Markets | 10% |

Plain-language takeaway: Credit Risk Measurement and Management is worth 20% of Part II (16 of 80 questions), per GARP's (Global Association of Risk Professionals) FRM study guide. That makes it one of the three largest topic weights on the exam.

That module covers credit scoring models, default-probability estimation, credit portfolio models, counterparty credit risk and related valuation adjustments. It is the theory layer underneath everything a credit risk modeler builds day to day.

An FRM candidate walks into a credit risk interview already fluent in the concepts. What they still need is hands-on model-building practice.

On exam logistics: FRM exams run at PSI test centers, across three windows a year — May, August and November. GARP charges a one-time enrollment fee on top of exam fees. For live dates and current fees, check our FRM exam dates hub instead of relying on a fixed number here, since GARP updates these periodically.

Recruiters recognise the credential specifically because it signals risk intent. Pairing it with actual PD/LGD/EAD (probability of default, loss given default, exposure at default) model-building experience is what turns that signal into an offer. Our is FRM worth it guide and FRM salaries in India guide cover the certification's broader value beyond credit risk specifically.

What Skills Do You Still Need to Add?

Neither a CA nor an FRM certificate teaches you to actually build a credit risk model end to end. Both qualifications give you strong foundations — but employers hire for hands-on modeling skill on top of that foundation, and that has to be added separately.

Four skill gaps show up in almost every job description for these roles:

- Spreadsheet and query skills. Excel is assumed everywhere — committees and reports still run on it. SQL (a language for pulling data out of databases) is how you get loan-book data out of a bank's systems in the first place.

- Python, and ideally some SAS awareness. On 5 July 2026, Indeed India keyword searches showed roughly 35,000 postings pairing Python with credit risk against about 5,000 for SAS — a 7:1 gap. Treat these as broad portal counts, not a formal survey, but the direction is clear: Python-first, SAS-aware is the safest combination.

- PD, LGD and EAD modeling in practice. Reading about probability of default is not the same as building a scorecard that estimates it from real data — this is the specific, buildable skill employers test for.

- ECL mechanics end to end. Staging a loan into Stage 1, 2 or 3, applying the 30-days-past-due trigger, and running the 12-month-versus-lifetime ECL calculation — the exact machinery RBI's directions now require every covered bank to run.

The good news: none of these four gaps require starting over. They sit on top of what a CA or FRM candidate already knows — they are additions, not replacements. Our companion posts on what credit risk modeling actually is and PD, LGD and EAD explained walk through this exact machinery in more depth.

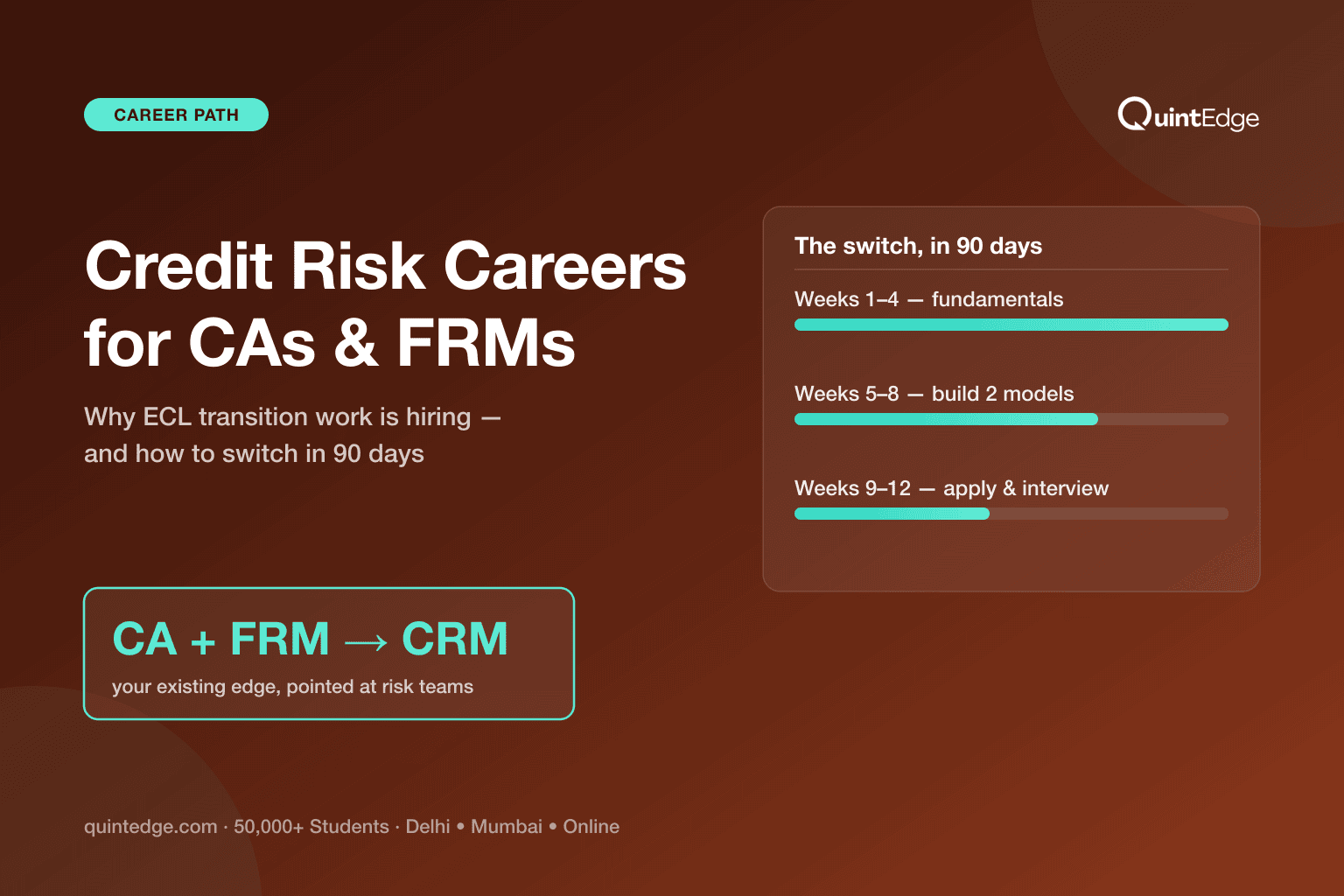

How Do You Switch in 90 Days?

A focused 90-day plan can take a CA or FRM candidate from "qualified in something adjacent" to "interview-ready for credit risk roles." The plan has three blocks. Learn the fundamentals, build proof of work, then apply and interview.

Weeks 1–4: Build the fundamentals.

- Learn the three core parameters — PD, LGD and EAD — and how they combine into expected loss (EL = PD × EAD × LGD).

- Learn the IFRS 9 / Ind AS 109 three-stage ECL framework — Stage 1, 2 and 3, and what triggers each one.

- Get comfortable with Python basics for data work — pandas for handling data, basic statistics for scoring models.

- Read RBI's ECL directions summary (27 April 2026, effective 1 April 2027) so the India-specific rules are not new vocabulary in an interview.

Weeks 5–8: Build two portfolio models.

- Build a PD scorecard end to end on a public lending dataset — data cleaning, logistic regression, and a chart showing how well it separates good borrowers from bad ones.

- Build a simple ECL calculation engine — stage a set of loans into Stage 1/2/3 and compute 12-month versus lifetime expected loss for each.

- Document both projects the way a bank would expect — assumptions written down, not just code. This is where CA-style documentation habits pay off directly.

Weeks 9–12: Apply and interview.

- Target roles across all three employer types — banks, Big 4 ECL-implementation teams, and GCC risk functions — since each values a slightly different mix of your background.

- Lead your CV and interview pitch with your portfolio projects, not just your qualification — one built model beats ten certificates in an interview room.

- Prepare the two nuances interviewers actually probe: why "12-month ECL" is not next year's expected loss, and why the significant-increase-in-credit-risk test tracks the change in default probability, not the change in loss amount.

- Practice explaining your CA or FRM background as a specific advantage for this role — accounting rigour or syllabus depth — rather than a generic qualification.

Frequently Asked Questions About Credit Risk Careers for CAs and FRMs

Yes. A CA's Ind AS 109 knowledge, financial-statement skills and audit-style documentation habits map directly onto ECL implementation, provisioning and model-validation work. Adding hands-on Python or SQL modeling skill on top of the CA is often enough for modeler and validator roles, especially at Big 4 firms and banks. FRM is a helpful add-on here, not a strict requirement.

It gets you an interview more easily, but not the job on its own. FRM Part II devotes 20% of its weight to Credit Risk Measurement and Management, so the theory is solid. But employers still test hands-on PD, LGD and EAD model-building skill in Python or SAS. Pair the certification with a built portfolio project for the strongest result.

Ind AS 109 is India's converged version of the global IFRS 9 accounting standard, notified under the Companies (Indian Accounting Standards) Rules, 2015. Larger NBFCs already compute expected credit losses under it. Banks are moving to a similar expected-credit-loss framework, but through RBI's own directions rather than Ind AS itself. The underlying logic, and the skills to work with it, are the same.

Not yet. Banks currently provision under the older incurred-loss method. RBI's final ECL directions, issued 27 April 2026, take effect from 1 April 2027, with the financial impact phased in through FY 2030–31. That gap between today and 2027 is precisely why banks are hiring credit risk talent now, before the deadline arrives.

We cannot give a fair general-CA comparison, since pay varies enormously by firm and role. What we can say: AmbitionBox estimates credit risk analysts in India earn ₹12.7–14 lakh per year in the typical experience band (1.8k salaries, updated 2 July 2026). Our credit risk analyst salary guide has the full breakdown by experience and employer type.

A focused 90-day plan is realistic for someone already CA-qualified or well into FRM prep. That means roughly four weeks on fundamentals, four weeks building two portfolio projects (a PD scorecard and an ECL engine), and four weeks on targeted applications and interviews. Working professionals studying part-time should expect this to stretch longer.

It depends on your target. If you want the strongest possible risk-specific signal for global banks or risk-management-titled roles, FRM's dedicated credit-risk module adds real value on top of a CA. If you are aiming at Big 4 ECL-implementation or audit-adjacent modeling work, hands-on Python and modeling skill may matter more than a second qualification. Our is FRM worth it guide covers this trade-off in depth.