ECL Model at a Glance

The IFRS 9 expected credit loss (ECL) model is an accounting rule that makes lenders set money aside for loan losses they expect in the future — not just losses that have already happened. Think of it as buying an umbrella before it rains, instead of only mopping the floor after.

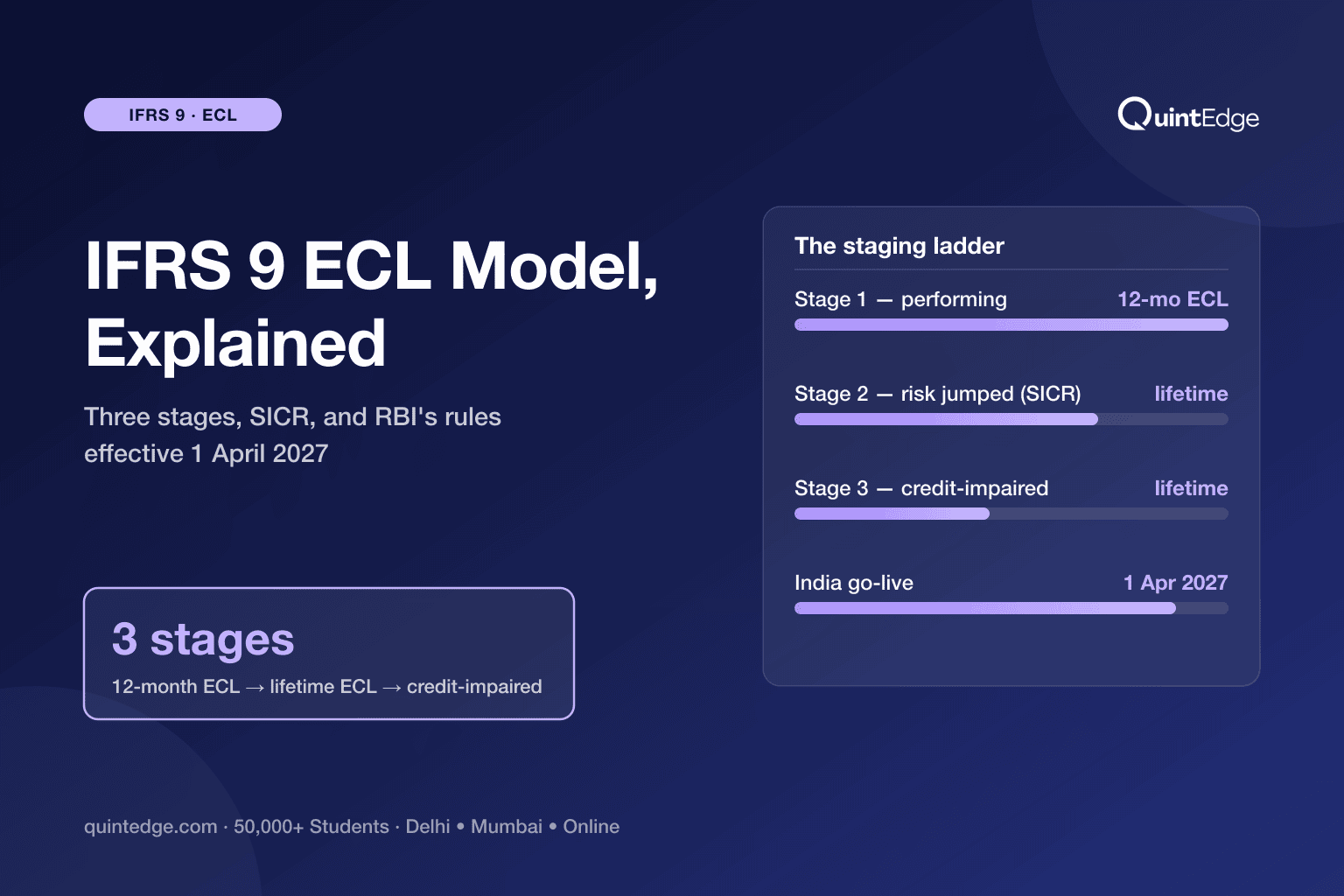

Every loan sits in one of three stages. Stage 1 is a healthy loan, so the bank sets aside 12 months of expected loss. Stage 2 is a loan whose risk has jumped — even with no missed payment yet — so the bank sets aside lifetime expected loss. Stage 3 is a loan that has actually gone bad, and it stays at lifetime loss.

India is now applying this logic to banks directly. On 27 April 2026, the Reserve Bank of India (RBI) issued final directions moving commercial banks to ECL provisioning from 1 April 2027, with the impact phased in through FY 2030–31. Larger NBFCs (non-banking finance companies) already work this way under a related rule, Ind AS 109, since 2018–19.

What Is Expected Credit Loss?

Expected credit loss (ECL) is the amount of money a lender expects to lose on a loan, estimated in advance and updated regularly — before any borrower actually misses a payment. It replaced an older rule that only let lenders provision after trouble was already visible.

That older rule was called the incurred-loss model. Under it, a bank could not set aside money for a loan until there was clear evidence of a problem — a missed payment, a covenant breach, a borrower in financial distress. Until that evidence showed up, the loan sat on the books as if nothing was wrong.

Regulators saw the flaw in the 2008 global financial crisis. Banks were holding almost no provisions right up to the moment loans started failing in bulk — because the incurred-loss rule does not look ahead. Losses that were building up quietly were invisible until it was too late to plan for them.

IFRS 9 — the global accounting standard — fixed this. It was issued by the International Accounting Standards Board (IASB) in July 2014 and became effective for periods starting on or after 1 January 2018. Under IFRS 9, lenders must recognise expected credit losses at all times, using past events, today's conditions and forecasts of what might happen next — and refresh that number every time they report results.

The everyday analogy is simple: an incurred-loss approach is like buying insurance only after your house has already flooded. An ECL approach is like buying the umbrella before it rains — you plan for the loss you can reasonably foresee, not just the one you can already see.

India's own accounting standard for this, Ind AS 109, is IFRS 9 converged into Indian rules under the Companies (Indian Accounting Standards) Rules, 2015. Large NBFCs already provision this way; banks are next, as covered below.

How Do the Three Stages Work?

IFRS 9 sorts every loan into one of three stages based on how its credit risk has changed since the loan began. The stage decides two things: how much provision the lender must hold, and how it recognises interest income.

| Stage | What triggers it | Provision required | Interest recognised on |

|---|---|---|---|

| Stage 1 — Performing | Loan is new, or risk has not risen significantly since it began | 12-month ECL | Full (gross) loan amount |

| Stage 2 — SICR | Significant increase in credit risk (SICR) since the loan began | Lifetime ECL | Full (gross) loan amount |

| Stage 3 — Credit-impaired | Loan is now considered credit-impaired | Lifetime ECL | Net amount (loan minus provision already set aside) |

In plain words: a Stage 1 loan is doing fine, so the bank only plans for losses that could hit in the next year. A Stage 2 loan is showing warning signs — no default yet, but risk has clearly risen — so the bank must now plan for losses over the loan's entire remaining life, not just one year. A Stage 3 loan is already in trouble, so the bank keeps the lifetime provision and stops counting interest on money it may never fully collect.

One nuance trips up almost everyone learning this for the first time. "12-month ECL" does not mean "losses expected in the next 12 months." It means: take the loan's full lifetime expected loss, and weight it by the chance that a default happens within the next 12 months. It is a slice of the lifetime number, not a separate 12-month forecast.

The move from Stage 1 to Stage 2 also does not require a missed payment. The test is whether the probability of default (PD — the chance the borrower fails to repay) has risen significantly since the loan started, even while every instalment is still being paid on time. That forward-looking test is what makes ECL fundamentally different from the old incurred-loss approach.

What Counts as a Significant Increase in Credit Risk?

A significant increase in credit risk (SICR) is a meaningful rise in the chance a borrower will default, measured over the loan's remaining life — checked at every reporting date, not just when a payment is missed. It is the trigger that moves a loan from Stage 1 to Stage 2.

The test looks at the change in the probability of default, not the change in the rupee amount that might be lost. A borrower's risk can rise sharply — a ratings downgrade, a stressed industry, a drop in income — well before any instalment is late. IFRS 9 requires lenders to catch that shift early, using past data, current conditions and forward-looking information together.

Because "significant" can be subjective, the rules provide one clear backstop: a rebuttable presumption that risk has increased significantly once a payment is more than 30 days past due. "Rebuttable" means a lender can argue against it with evidence, but by default, 30-plus days late puts a loan into Stage 2.

It helps to separate two dates that often get confused. The 30-days-past-due marker is about early warning — it moves a loan into heavier provisioning while it may still be recoverable. The 90-days-past-due marker is India's long-standing definition of an actual non-performing asset (NPA — a loan the bank formally treats as in default). RBI's directions keep the NPA line at 90+ days even as ECL staging adds the earlier 30-day checkpoint.

| Checkpoint | Days overdue | What it triggers |

|---|---|---|

| SICR presumption | 30+ days past due (rebuttable) | Loan moves to Stage 2 — lifetime ECL provisioning |

| NPA classification | 90+ days past due | Loan is formally classified as non-performing (unchanged by the new ECL rules) |

One sentence to take away: 30 days is an early-warning trigger for provisioning; 90 days is still the line for calling a loan a formal default. The two checkpoints work together, not against each other.

What Did RBI's April 2026 Directions Change?

On 27 April 2026, RBI issued final directions moving Indian commercial banks from their old loss-provisioning rule to an IFRS 9-style, three-stage ECL framework — the biggest change to bank provisioning in decades. The rules take effect from 1 April 2027, with the balance-sheet impact allowed to phase in through FY 2030–31.

The official name is the "Reserve Bank of India (Commercial Banks – Asset Classification, Provisioning and Income Recognition) Directions, 2026" (circular RBI/DOR/2026-27/398, dated 27 April 2026). RBI's own press release states plainly: "These Directions shall come into effect from April 01, 2027." This followed a draft version released for public feedback on 7 October 2025, with the final version incorporating industry comments.

| Milestone | Date |

|---|---|

| Discussion paper | January 2023 |

| Draft directions released for feedback | 7 October 2025 |

| Final directions issued | 27 April 2026 |

| Framework goes live | 1 April 2027 |

| Phase-in of full impact complete | FY 2030–31 |

Who is covered: the directions apply to commercial banks — excluding small finance banks, payments banks and local area banks — plus the State Bank of India and other corresponding new banks. Co-operative banks are not covered by these ECL directions (a separate, unrelated stressed-assets rule touches urban co-operative banks). All India Financial Institutions get their own directions, issued separately.

The mechanics mirror the IFRS 9 three-stage model you just read above — the same 12-month/lifetime split, the same 30-day SICR presumption, the same 90-day NPA line. RBI's directions add a few India-specific guardrails on top:

- Prudential floors. RBI has set product-wise minimum provisioning floors for Stage 1 and Stage 2 loans, acting as regulatory backstops — a bank's own model can never provision below these floors, however low its estimate.

- Board oversight. A bank's Board of Directors is responsible for overseeing the ECL framework, typically through a designated committee.

- One-time transition. On 1 April 2027, banks must fair-value their entire loan portfolio; the difference goes straight to opening retained earnings rather than through the profit-and-loss account — which is exactly why the impact is allowed to phase in over four years, out to FY 2030–31.

Why is a four-year runway needed at all? Because banks are currently provisioning under the older incurred-loss approach and have never held Stage 2-style lifetime provisions before — moving straight to the new floors in one year would strain capital. Independent credit-rating agency ICRA assessed the change on 30 April 2026 in a report titled "RBI releases final ECL framework; impact on banks' capitalisation profile likely to be moderate."

How Is This Different From What NBFCs Already Do?

Large NBFCs (non-banking finance companies) in India are not new to this — they have provisioned under ECL logic for years. The gap RBI's directions close is specifically a bank gap, and understanding that gap is what makes this whole topic a hiring story rather than old news.

NBFCs that adopted Ind AS (India's IFRS-converged accounting rules) already compute expected credit losses under Ind AS 109 — the same three-stage logic covered above. The timeline: NBFCs with net worth of ₹500 crore or more adopted Ind AS from FY 2018–19; other covered NBFCs followed from FY 2019–20. RBI layered its own guardrails on top in March 2020 — board-approved ECL methodologies, documented assumptions, and an Impairment Reserve that NBFCs must maintain wherever their ECL provision comes in lower than what the older provisioning rule would have required.

Banks have been on a different track entirely. Scheduled commercial banks were not required to move to Ind AS — RBI deferred that transition for banks pending legislative changes — so banks have continued provisioning under the older incurred-loss regime that ECL is now replacing. That is precisely why the April 2026 directions matter: banks are jumping from "no ECL" to "full three-stage ECL" in one regulatory move, while NBFCs made a similar jump years ago under a different rule (Ind AS 109) with more runway.

| Larger NBFCs | Commercial banks | |

|---|---|---|

| ECL rule | Ind AS 109 | RBI's Commercial Banks Directions, 2026 |

| Already using ECL? | Yes, since FY 2018–19 / FY 2019–20 | Not yet — still on incurred-loss until 1 April 2027 |

| Extra guardrail | Impairment Reserve if ECL < old provisioning | Product-wise prudential floors on Stage 1/2 |

For anyone building a career here, this is good news, not a red flag: it means Indian NBFCs already run live ECL teams you can learn from and benchmark against, while banks are about to build theirs from scratch — creating a wave of new roles at the exact moment demand for this skill peaks.

What Does This Mean for Jobs in India?

Every commercial bank covered by RBI's directions must build, test and run compliant ECL models before 1 April 2027 — and then keep maintaining them permanently. That is a fixed, dated deadline forcing hiring across banks, NBFCs, Big 4 consulting practices and global capability centres (GCCs — offshore teams that global banks run out of India) all at once.

The backdrop makes this a build-out story, not a distress story. Gross NPAs (non-performing assets) at Indian banks touched a multi-decadal low of 1.8% in March 2026, according to RBI's Financial Stability Report released on 30 June 2026. Clean loan books are not a reason to shrink risk teams — they are the result of exactly this kind of disciplined measurement, and the new ECL regime raises that bar further rather than lowering it.

The transition itself is what creates the roles. Someone has to build the PD, LGD and EAD (probability of default, loss given default, exposure at default — the three inputs to any ECL number) models; someone has to decide what counts as a significant increase in credit risk for each product; someone has to validate that the floors and governance rules are followed; and someone has to document all of it for the board and for RBI's supervisors.

On pay, we track this in detail elsewhere so the numbers stay current: AmbitionBox estimates credit risk analysts in India earn ₹12.7–14 lakh per year (1.8k reported salaries, updated 2 July 2026), and our credit risk analyst salary in India guide breaks this down further by experience level and employer type.

Frequently Asked Questions About IFRS 9 and ECL

ECL stands for expected credit loss. It is the amount of money a bank or NBFC expects to lose on a loan, estimated ahead of time using past data, current conditions and forecasts — rather than waiting until a borrower has already missed a payment. IFRS 9 is the accounting standard that made this method mandatory worldwide.

12-month ECL is the slice of a loan's total lifetime expected loss that relates to a default happening in the next 12 months — it is not a separate one-year forecast. Lifetime ECL covers expected losses over the loan's entire remaining life. Stage 1 loans get 12-month ECL; Stage 2 and Stage 3 loans get lifetime ECL because their risk has risen or they have already defaulted.

No — a loan can move to Stage 2 without any missed payment, purely because its probability of default has risen significantly (a ratings downgrade or a stressed sector, for example). Separately, India's rules apply a rebuttable presumption that risk has risen significantly once a payment is more than 30 days past due — but that is a backstop, not the only trigger.

No. RBI's final directions keep the non-performing asset (NPA) definition at more than 90 days past due, exactly as before. The new 30-days-past-due checkpoint is a separate, earlier trigger that only affects ECL staging and provisioning — it does not change when a loan is formally classified as non-performing.

Commercial banks, including the State Bank of India and other corresponding new banks — but excluding small finance banks, payments banks and local area banks. Co-operative banks are not covered by these ECL directions either. All India Financial Institutions will get their own separate directions.

Banks are moving straight from the older incurred-loss provisioning rule to full three-stage ECL, including new prudential floors — a bigger one-time jump than NBFCs faced under Ind AS 109. RBI is letting banks spread the profitability and capital impact over roughly four years, from the 1 April 2027 start to FY 2030–31, so the transition does not strain capital in a single reporting period.

You need to understand the PD, LGD and EAD parameters that feed into every ECL number, be comfortable in Python or SQL to build and test the models, and know the IFRS 9 / RBI staging rules well enough to explain why a loan sits in a given stage. Our PD, LGD and EAD guide and credit risk modeling overview cover the foundations in order.