Python or SAS: The Quick Answer

For a fresher targeting credit-risk roles in India in 2026: learn Python first, learn to read SAS second. Python is where new model development, validation and analytics work is going — and it is free to learn at home. SAS still runs a huge share of the models already in production inside banks, so the ability to read and translate SAS code makes you useful from day one.

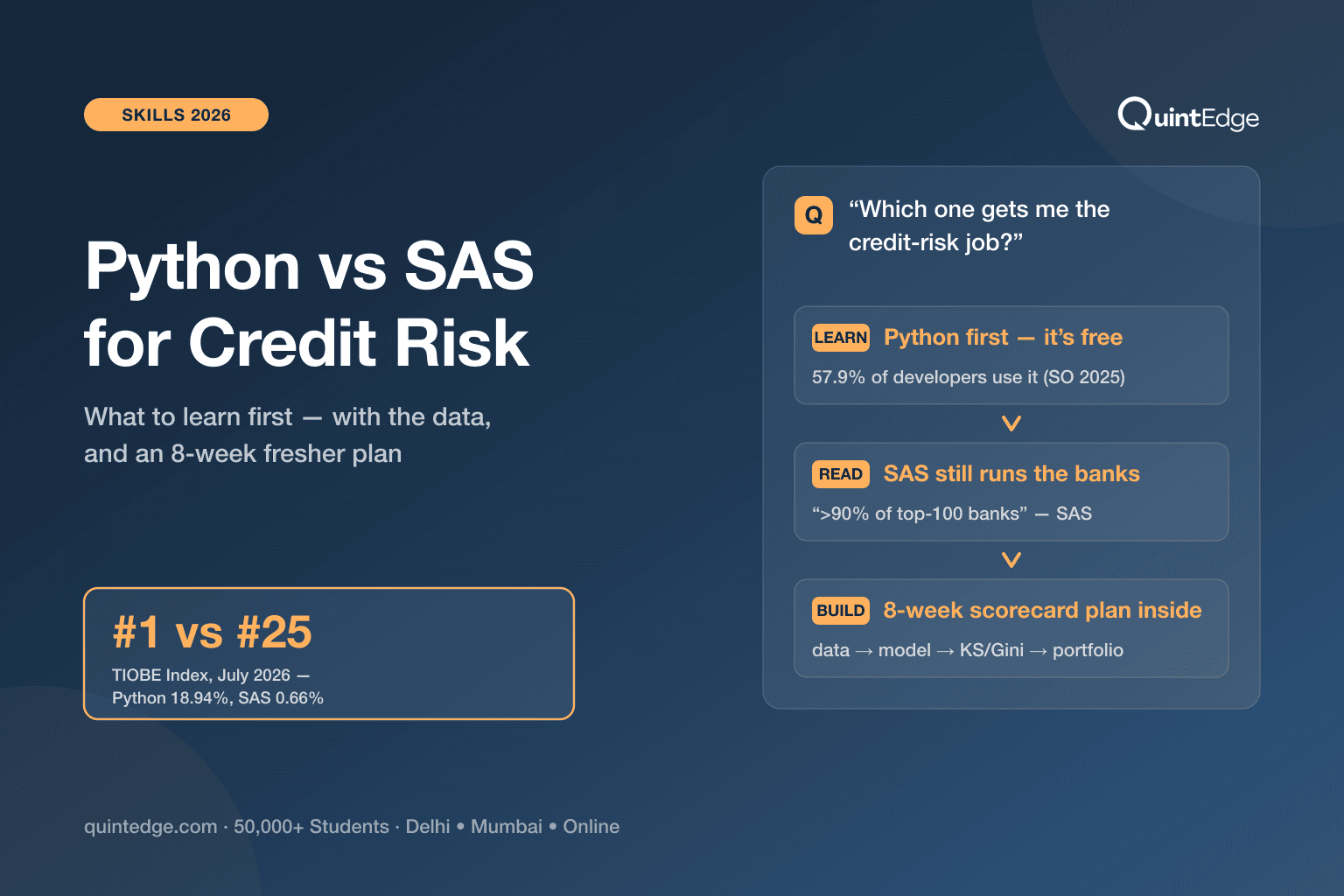

The evidence for that split, in two numbers you can quote: Python sits at #1 on the TIOBE index (18.94%, July 2026) while SAS sits at #25 (0.66%) — yet SAS itself reports that over 90% of the world's top 100 banks use its software (sas.com, checked July 2026). New work flows one way; installed systems point the other. Your strategy has to respect both.

Why Do Banks Still Run SAS?

SAS is a commercial analytics platform — language plus software — that banks adopted decades before Python was credible in finance. Entire generations of credit scorecards, provisioning engines and regulatory reports were built, tested and audited in it.

SAS's own banking page claims ">90% of the top 100 largest global banks" as customers, across 1,600+ banks in 92 countries (SAS's published figures, checked July 2026 — the vendor's claim, but a credible one).

Banks keep it for reasons that make sense once you think like a regulator, not a developer:

- Validated history. A production PD model — the kind explained in our PD-LGD-EAD guide — passed years of audits in SAS. Rebuilding it elsewhere means re-validating everything, at real cost and model risk.

- Audit trails by design. SAS ships with logging, access control and lineage that auditors already trust. With Python, the bank must assemble that governance itself.

- Vendor accountability. When a regulator questions the platform, there is a company to answer. Open-source has no throat to choke — a real consideration in regulated industries.

- Working code is expensive to retire. The migration only happens when the business case forces it — which, with the ECL transition, is now genuinely happening in many places, team by team.

The catch for freshers: SAS licences cost employers real money, so you cannot legally run full SAS at home the way you run Python. That single fact shapes the learning strategy in this post.

Why Is Python Winning the New Work?

Three forces, each with a named number behind it:

| Signal | Python | SAS | Source (as of July 2026) |

|---|---|---|---|

| Language popularity | #1, rating 18.94% | #25, rating 0.66% | TIOBE Index, July 2026 |

| Developers using it | 57.9% of respondents (up 7 points in a year); 71.8% among learners | Not in the top tier | Stack Overflow Developer Survey 2025 |

| Cost to learn & run | Free, open-source | Commercial licence via employer | — |

| Installed base in banking | Growing | ">90% of the top 100 largest global banks" — the vendor's own claim | sas.com banking page |

Plain takeaway: every forward-looking indicator points to Python; the one backward-looking indicator — what is already installed — points to SAS. That is not a contradiction. It is a job description: banks need people who can build the future stack while reading the installed one.

The ecosystem argument matters more than the popularity contest. Modern credit-risk work leans on pandas (data handling), scikit-learn (models), and open validation tooling — plus the entire machine-learning world when you need it.

And the timing is Indian-specific: the RBI's expected-credit-loss directions (final, 27 April 2026; effective 1 April 2027) have banks building and re-validating loss models on a deadline — see our ECL model guide — and much of that new build is happening in Python while the legacy being replaced sits in SAS.

What Does a Credit-Risk Team Actually Use Them For?

Strip the jargon and a credit-risk modelling team does five things. Here is where each language sits today:

| Stage | What it means in plain words | Typical tool today |

|---|---|---|

| 1. Data preparation | Pull loan histories, clean them, build features (income, past dues, utilisation) | SQL everywhere; Python (pandas) or SAS data steps |

| 2. Model build | Fit PD/LGD/EAD models — scorecards that estimate default and loss | Python increasingly; SAS in legacy rebuilds |

| 3. Validation | Independently re-test the model: does it separate good from bad? (KS, Gini), is it stable? (PSI) | Python for challengers; SAS to replicate production |

| 4. Deployment | Wire the model into live lending decisions and ECL provisioning | Bank's platform — often still SAS-based |

| 5. Monitoring | Watch the model monthly; raise flags when the population drifts | Whatever deployment used, plus Python dashboards |

Plain takeaway: Python dominates stages 2–3 (where freshers are hired), SAS lingers in 4–5 (where production lives). The three metrics named above — KS and Gini for "does the model rank risk correctly", PSI for "has the incoming population drifted from the build data" — are the vocabulary of both worlds, and they are language-independent ideas. Learn the idea; the syntax is an afternoon.

The concepts underneath all five stages are covered in what is credit risk modeling; the interview versions live in credit-risk interview questions.

Which Should a Fresher Learn First in 2026?

Python — and the reasoning is practical, not fashionable:

- You can practise tonight, free. Python, pandas, scikit-learn and public loan datasets cost nothing. SAS practice realistically requires an employer's licence — you cannot build a portfolio in a tool you cannot run.

- Interviews test doing. A fresher who walks in with a built-and-validated scorecard project beats one who lists "SAS (familiar)" on a CV every time.

- The skill transfers down, not up. Python-first analysts pick up read-level SAS in weeks (the figure above shows why). SAS-first freshers without Python face the harder climb — and the job ads increasingly lead with Python.

Adjust only by employer type: PSU banks and older insurers lean SAS-heavy, so read-level SAS matters more there; GCCs, NBFCs and fintechs are Python-first; Big 4 risk consulting expects both flavours of literacy. In every case the order stays the same — Python to build, SAS to read.

The 8-Week Python-for-Credit-Risk Plan

This plan assumes 8–10 hours a week and zero coding background. Each fortnight ends with a gate — a concrete "can you do this?" test. If you fail a gate, repeat that fortnight before moving on; do not carry debt forward.

| Weeks | Build | Gate at the end |

|---|---|---|

| 1–2 | Python basics: variables, lists, functions, loops. Then pandas: load a CSV, filter rows, group and summarise | Given a raw loans CSV, produce average loan size and default rate by city — without help |

| 3–4 | Explore a public lending dataset: missing values, outliers, simple charts. Build features (payment history, utilisation) | Write a one-page note: which 5 variables predict default here, with evidence |

| 5–6 | Fit a logistic-regression scorecard in scikit-learn. Score the portfolio. Compute KS and Gini yourself, then PSI between two periods | Explain to a non-coder what your Gini means, and whether the model is usable |

| 7 | SQL joins + read-level SAS: translate five PROC/DATA-step snippets into pandas equivalents | Given a SAS scorecard snippet, say in plain English what it does |

| 8 | Package one project end-to-end: data → model → validation metrics → 2-page write-up, on GitHub | A friend can run your notebook top to bottom without you in the room |

Plain takeaway: eight honest weeks produce the exact artefact credit-risk interviewers ask about — a built, validated, documented scorecard — plus the SAS-reading party trick most freshers skip.

Fall-behind rule: if a week slips, cut scope, not gates — use a smaller dataset and fewer features, but never skip computing KS/Gini/PSI yourself. The metrics are the employable part.

Will AI Coding Tools Replace Both Languages?

AI assistants now write serviceable Python and translate SAS competently — which changes the job, not the need. Banks cannot deploy a model because a chatbot wrote it: someone accountable must choose the method, check the data, defend the validation and sign the documentation.

The RBI's ECL directions explicitly demand governance around model risk, and its draft circular on credit-model risk management (August 2024 — still a draft) pushes the same way: independent validation, at least yearly. Machines draft; humans remain answerable.

Practically, AI tools make the Python-first strategy stronger — they flatten the syntax learning curve, so the differentiator shifts to exactly what this plan gates: understanding why a scorecard works, when it does not, and how to prove it. We take the wider question on directly in will AI replace finance jobs.

Python vs SAS for Credit Risk: Frequently Asked Questions

Learn Python to working depth and SAS to reading depth — that combination covers the 2026 Indian market. Write-level SAS is worth adding only when an employer's stack demands it, at which point they provide the licence and the codebase to learn from. Listing honest read-level SAS on a CV is both truthful and valued.

Its share of new work is clearly shrinking — TIOBE places it at #25 with a 0.66% rating in July 2026 — but its installed base is enormous: SAS itself claims over 90% of the top 100 global banks. Production systems retire slowly in regulated industries. Expect SAS to fade over years inside banks, not vanish — which is precisely why read-level SAS remains employable.

Everything in the 8-week plan runs on free tools: Python and pandas cost nothing, scikit-learn is open-source, and public lending datasets are widely available for exactly this kind of practice. A laptop and eight honest weeks produce a portfolio project — no paid course or licence is required to reach interview-ready.

No — both are concept exams answered on multiple-choice screens, not coding tests. But the roles those certifications target increasingly screen for Python separately. The strong fresher profile in credit risk pairs a concept credential like the FRM with a demonstrable Python project; each covers the other's blind spot.

Only as a second tool where a specific team already uses it. The 2025 Stack Overflow survey puts R at 4.9% of developers against Python's 57.9%, and Indian credit-risk job ads reflect the same gap. R remains excellent for statistics, but as a fresher's first bet it narrows your market rather than widening it.

Enough to read a DATA step and the common PROCs (MEANS, FREQ, SORT, LOGISTIC) and explain in plain English what a snippet does — week 7 of the plan above. That level lets you honestly say you can work with legacy code from day one. Claiming more than you can demonstrate is the one move that reliably backfires in technical rounds.