What Are the Basel Norms?

The Basel norms are the global rulebook for how much loss-absorbing capital a bank must hold against the risks it takes. They are written by the Basel Committee on Banking Supervision (BCBS) — a club of central banks and regulators that meets at the Bank for International Settlements in Basel, Switzerland — and enforced in India by the RBI, usually in a stricter form.

Think of them as seatbelt laws for banks. A seatbelt does not stop the crash; it stops the crash from killing you. Capital does not stop loans going bad; it makes sure the bank — and your deposit — survives when they do. Each generation of the rules (Basel I, II, III, and now the "endgame") is a better seatbelt, designed after studying the last crash.

If you are heading into any bank, credit-risk or FRM interview, Basel is not optional trivia. It decides how much lending a bank can do, how loans are priced, and why entire teams exist to compute one ratio correctly.

Why Do Banks Need Capital Rules at All?

Because a bank runs almost entirely on other people's money. Here is a toy bank, with small round numbers (illustrative):

| What the bank owns (assets) | ₹ | Where the money came from | ₹ |

|---|---|---|---|

| Loans given out | 90 | Customer deposits (owed back!) | 92 |

| Cash and bonds | 10 | Owners' capital (equity) | 8 |

| Total | 100 | Total | 100 |

Plain takeaway: of every ₹100 this bank deploys, only ₹8 is its own. The other ₹92 belongs to depositors, who can ask for it back.

Now let borrowers worth ₹5 default and repay nothing. The loss lands on the owners' ₹8 first — capital absorbs it, and depositors stay whole. But if losses reach ₹9, capital is wiped out and the bank cannot repay everyone. Depositors panic, queues form, and the failure spreads to other banks that lent to it. That domino effect is why bank capital is a public concern, not a private choice.

The committee itself was born from exactly such a domino. In June 1974, Germany's Bankhaus Herstatt collapsed mid-settlement, leaving banks across the world unpaid. By the end of 1974 the G10 central banks had formed the Basel Committee (BIS history, checked July 2026). Every Basel accord since has followed the same pattern: crisis first, rulebook after.

What Did Basel I Do? (1988)

Basel I, the first Capital Accord (July 1988), introduced the idea the whole system still runs on: risk-weighted assets (RWA). Not every ₹100 of assets is equally dangerous, so each asset gets a risk weight — a danger multiplier — and capital is required as a percentage of the weighted total, not the raw total. The rule: capital ≥ 8% of RWA, to be met by end-1992 (BIS).

Worked example (illustrative, Basel I-style weights):

| Asset | Amount | Risk weight | RWA |

|---|---|---|---|

| Government bonds | ₹40 | 0% | ₹0 |

| Home loans (mortgages) | ₹20 | 50% | ₹10 |

| Corporate loans | ₹40 | 100% | ₹40 |

| Total | ₹100 | — | ₹50 |

Plain takeaway: ₹100 of assets shrinks to ₹50 of risk-weighted assets, so this bank needs 8% × ₹50 = ₹4 of capital. Lending to the government needs no cushion; lending to companies needs the full one.

Basel I's genius was simplicity. Its flaw was the same thing: with only a handful of weight buckets, a loan to a shaky startup and a loan to a blue-chip both weighed 100%. Banks learned to game the buckets — real risk crept up while measured risk stayed flat.

What Did Basel II Add? (2004)

Basel II (June 2004) replaced the blunt buckets with sensitivity, and organised supervision into three pillars — three questions a regulator keeps asking every bank:

- Pillar 1 — "Are you holding the minimum?" Capital rules now covering credit, market and operational risk. Big banks could use internal models (the IRB approach) to estimate their own inputs — the PD, LGD and EAD numbers explained in our PD-LGD-EAD guide — instead of flat weights.

- Pillar 2 — "What about the risks the formulas miss?" A supervisory review of everything Pillar 1 cannot see: concentration, interest-rate risk in the banking book, governance.

- Pillar 3 — "Now show the public." Mandatory disclosures so markets can judge a bank's risk themselves. Those Basel disclosure PDFs on every bank's website? That is Pillar 3.

Then 2008 happened. Banks that were "well-capitalised" on Basel II arithmetic failed anyway — capital was too thin and too low-quality, internal models had been optimistic, and nobody had rules for the risk that actually killed banks that year: running out of cash. The crisis exposed the gap between measured risk and real risk — and wrote the agenda for Basel III.

What Did Basel III Change After 2008? (2010)

Basel III (December 2010, phased 2013–2019 globally per BIS) rebuilt the seatbelt on four fronts. Each one answers a specific 2008 failure:

| Fix | What it means in plain words | Global minimum |

|---|---|---|

| Better capital (CET1) | Count mostly real shareholder money — Common Equity Tier 1 — not clever hybrid instruments that vanished in the crisis | CET1 ≥ 4.5% of RWA (within total capital ≥ 8%) |

| Buffers on top | A capital conservation buffer (CCB) for bad years, plus a countercyclical buffer (CCyB) regulators can switch on in booms | CCB 2.5% · CCyB 0–2.5% |

| Leverage ratio | A backstop that ignores risk weights entirely: capital versus total exposure, in case the weights are wrong | ≥ 3% |

| Liquidity rules | LCR: enough sellable assets to survive 30 days of stress. NSFR: fund long-term assets with stable money, not overnight borrowing | Both ≥ 100% |

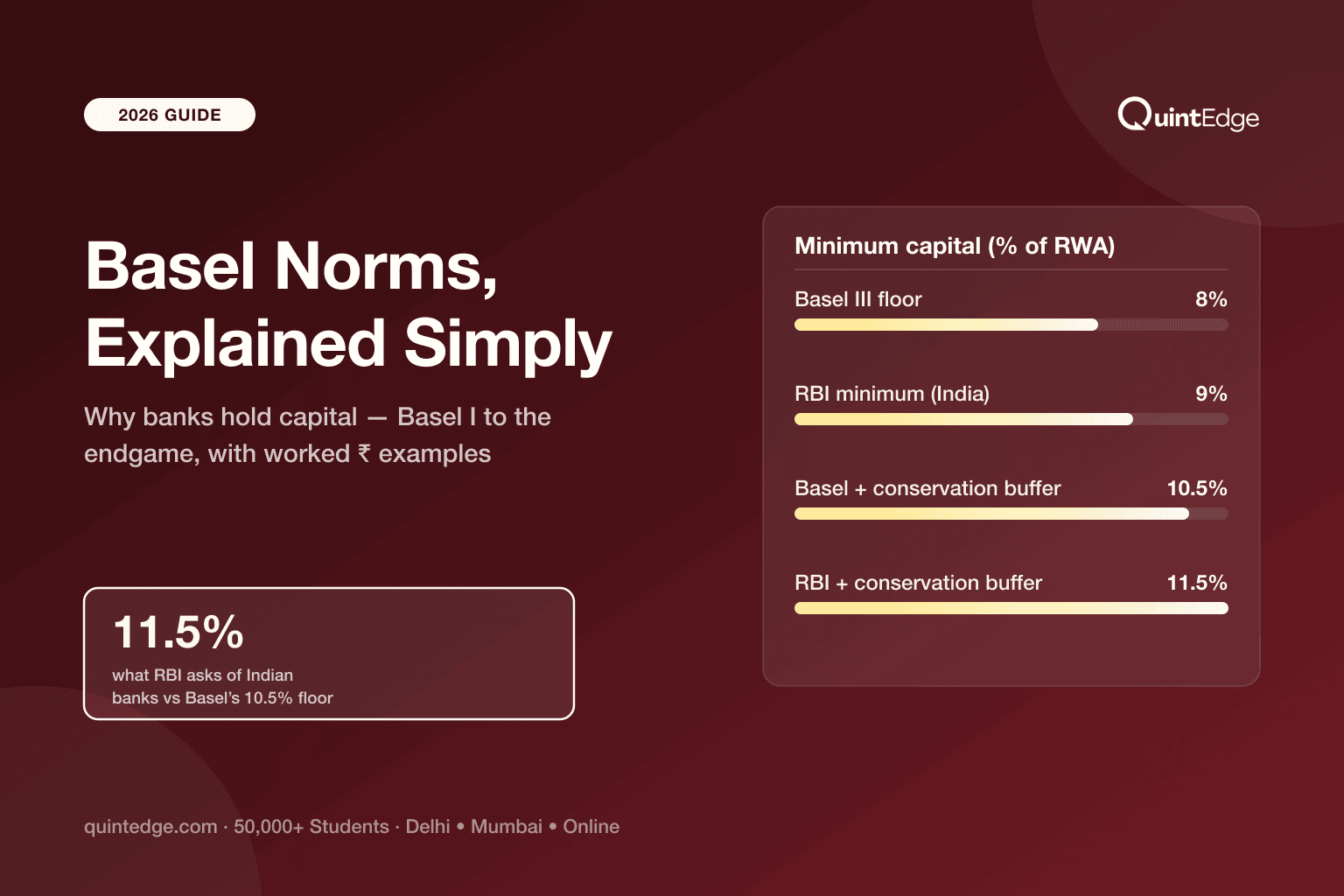

Plain takeaway: Basel III made capital bigger and more real, added rainy-day buffers, put a simple backstop under the clever maths, and — for the first time — regulated cash survival, not just solvency.

The buffers deserve one plain sentence each. The CCB works like a phone's battery-saver zone: dip into the last 2.5% and you survive, but the rules restrict dividends and bonuses until you recharge. The CCyB is a boom-time brake: regulators can demand extra capital when credit grows too fast, building cushion exactly when banks feel invincible.

What Is the "Basel III Endgame" Everyone Mentions?

In December 2017 the committee finalised the last block of post-crisis reforms — officially "the finalisation of Basel III", informally Basel 3.1, Basel IV or the endgame. Its centrepiece attacks the internal-model problem directly: the output floor.

The floor in one worked example (illustrative): a big bank's internal models say its portfolio needs RWA of ₹60 crore; the regulator's standardised formulas say ₹100 crore.

Under the floor, the bank must compute capital on at least 72.5% of the standardised answer — ₹72.5 crore — no matter what its models claim. Models can still earn a discount, but never a bottomless one. The floor phases up to its full 72.5% by 1 January 2028 (BIS revised timeline, March 2020).

Where the world actually stands as of July 2026 — a favourite interview question:

| Jurisdiction | Status (July 2026) | Key dates |

|---|---|---|

| UK | Final rules published (PRA policy statement PS1/26, January 2026) | Live 1 Jan 2027; market-risk internal models (FRTB-IMA) deferred to 1 Jan 2028 |

| EU | Core package (CRR3) live since January 2025 | Market-risk piece (FRTB) postponed by the Commission to 1 Jan 2027 |

| US | Re-proposed March 2026 after pushback on the 2023 draft (comments closed 18 June 2026) | Final rule expected late 2026; implementation ~2027 (industry expectation per Bloomberg/PwC coverage) |

| India | RBI runs Basel III with stricter minimums; adoption of revised approaches follows RBI's own calendar | See the India section below |

Plain takeaway: the endgame is law-in-motion, not history — the UK and EU converge on 2027, the US is still finalising, and the output floor completes globally in 2028. Saying exactly this, with dates, is an instant credibility marker in interviews.

How Does India Apply Basel Norms?

The RBI adopts the Basel framework but sets several dials tighter — India learned from other people's crises. The numbers every interview candidate should hold (RBI Master Circular on Basel III Capital Regulations; D-SIB list December 2025; checked July 2026):

| Requirement | Basel III global floor | RBI (India) |

|---|---|---|

| Minimum total capital (CRAR) | 8% of RWA | 9% of RWA |

| Minimum CET1 | 4.5% | 5.5% |

| Capital conservation buffer | 2.5% | 2.5% |

| Effective total with buffer | 10.5% | 11.5% (CET1-heavy: 8% CET1) |

| Countercyclical buffer (CCyB) | 0–2.5%, jurisdiction's call | Framework since 2015, never activated — kept at 0% at the May 2026 review |

Plain takeaway: an Indian bank needs ₹11.50 of capital for every ₹100 of risk-weighted assets — a full percentage point more than the global floor, with more of it in hard equity.

Three more India-specific pieces complete the picture:

- D-SIB surcharges. Banks "too big to fail" carry extra CET1. The RBI's December 2025 list (data as on 31 March 2025): SBI +0.80%, HDFC Bank +0.40%, ICICI Bank +0.20%. For SBI, the CET1 requirement alone becomes 5.5 + 2.5 + 0.8 = 8.8%.

- The provisioning revolution. Capital is the cushion for unexpected losses; provisions cover the expected ones. Here India just made its biggest move in decades: the RBI's final directions of 27 April 2026 shift banks from incurred-loss provisioning to a forward-looking expected credit loss (ECL) regime from 1 April 2027, with a glide path to 31 March 2031 for the extra provisions. Full mechanics in our IFRS 9 / ECL model guide.

- Disclosure. Every Indian bank publishes quarterly Basel III (Pillar 3) disclosures — the same documents risk teams help prepare, and the best free study material on how the rules bite a real balance sheet.

Why Do Basel Norms Matter for Your Career?

Because they generate jobs — thousands of them. Someone must compute RWA correctly across millions of loans, build and re-validate the PD/LGD/EAD models behind IRB and ECL numbers, run the liquidity ratios daily, prepare Pillar 3 disclosures, and re-plan capital every time a rule moves. That "someone" is a stack of teams: regulatory reporting, credit-risk modelling, model validation, capital planning, treasury risk.

The 2026–28 window is unusually good for entering this lane in India: the ECL transition alone has banks and consultancies staffing up model-build and model-validation teams, and every model in that pipeline needs tooling — the Python-vs-SAS question — and people who can defend numbers to auditors and the RBI. Basel is also core syllabus in the FRM, which is why risk interviewers probe it so confidently.

Start with the concepts behind the ratios — what credit risk modeling is and PD, LGD & EAD — then rehearse the numbers from this page against real credit-risk interview questions.

Basel Norms: Frequently Asked Questions

CRAR — the Capital to Risk-weighted Assets Ratio — is the bank's cushion expressed as a percentage of its danger-adjusted assets. Take the bank's capital, divide by risk-weighted assets, and compare against the minimum. In India that minimum is 9%, and 11.5% once the conservation buffer is included, versus the Basel global floor of 8% and 10.5%.

The core Basel III capital and liquidity framework has been live in India for years, at stricter-than-global levels — 9% minimum CRAR against Basel's 8%. The 2017 "endgame" refinements follow the RBI's own adoption calendar rather than a single global date. India's big current transition is on the provisioning side: the expected credit loss directions issued on 27 April 2026, effective from 1 April 2027.

Basel sets floors, not ceilings — any regulator can demand more, and the RBI deliberately does. A thicker cushion suits a banking system with concentrated corporate exposures and a history of bad-loan cycles. The same conservatism shows up elsewhere: a higher CET1 minimum of 5.5%, and D-SIB surcharges on SBI, HDFC Bank and ICICI Bank.

It is the rule that a bank's internal models can never push its risk-weighted assets below 72.5% of what the regulator's standardised formulas would say. Models may earn a discount on capital, but never a bottomless one — that caps the model-gaming problem that Basel II exposed. The floor phases in fully by 1 January 2028.

Not officially. The Basel Committee calls the December 2017 package "the finalisation of Basel III". The industry nicknamed it Basel IV, Basel 3.1 or the endgame because its changes — revised standardised approaches, constraints on internal models and the output floor — felt big enough to deserve a new number. In an interview, use "finalisation of Basel III" and mention the nicknames.

Not the full bank framework. NBFCs follow the RBI's separate scale-based regulation, which borrows Basel ideas — capital adequacy ratios, governance expectations — with thresholds set for non-bank lenders. The concepts you learn here transfer directly, which is why NBFC credit-risk teams interview on Basel logic even though the exact rulebook differs.