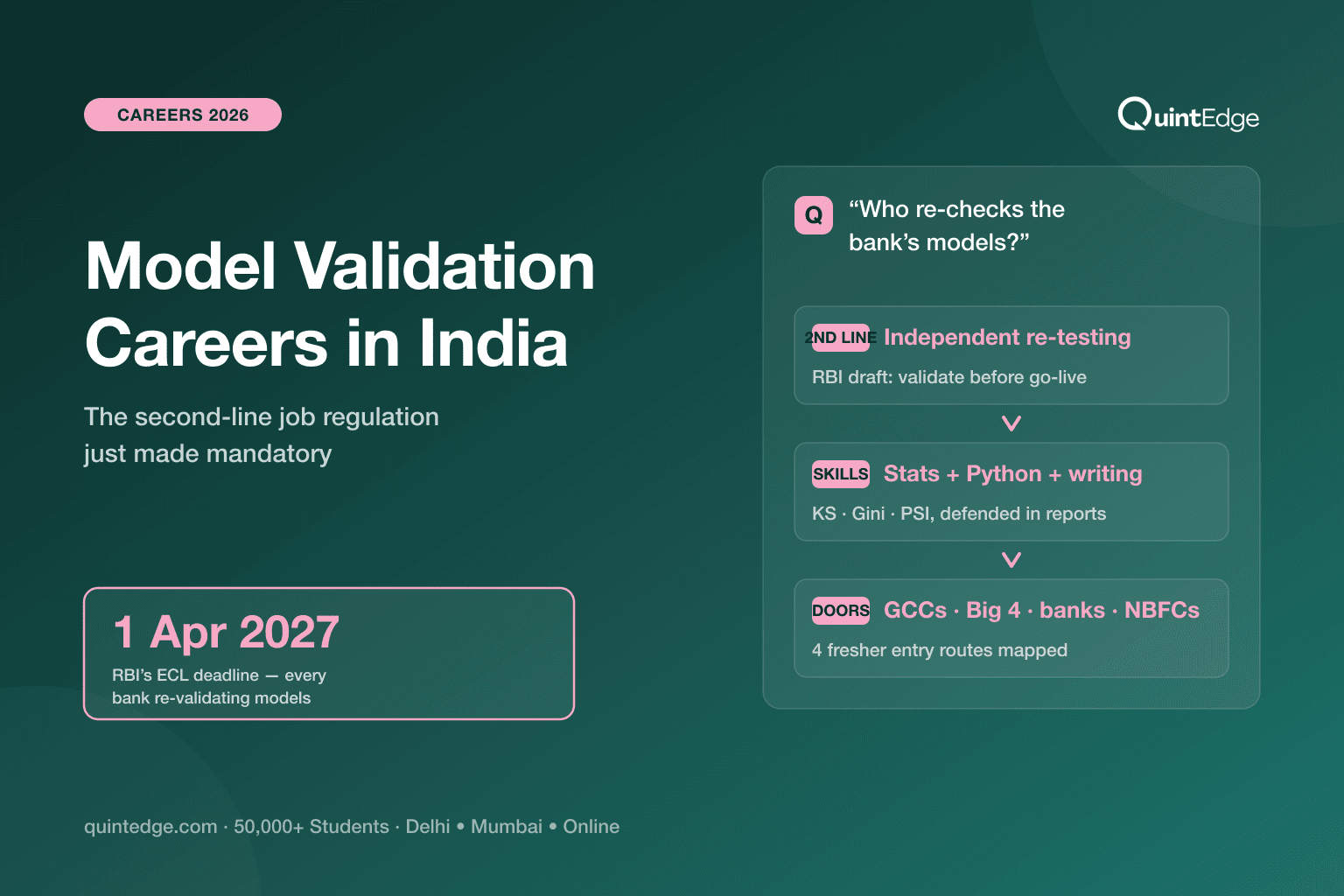

What Is Model Validation?

Model validation is the job of independently re-checking a bank's models — before they go live, and again every year they stay live. A bank today runs on models: who gets a loan (credit scorecards), how much loss to provision for (ECL models), how much capital to hold.

A wrong model quietly mis-prices thousands of decisions. The validator's job is to catch it before the regulator — or the loss — does.

Think of it as the second-opinion doctor. The treating doctor (the model developer) is skilled and well-meaning — but the hospital still wants an independent specialist to re-read the scans before major surgery. Not because the first doctor is bad; because the stakes forbid unchecked judgement. Validation is that second opinion, done with data, statistics and a written verdict.

In risk-team org charts this sits in the second line of defence — separate from the model builders (first line) and from internal audit (third line). Separation is the whole point: you cannot mark your own homework.

Why Is This Job Growing in India Right Now?

Three regulatory currents are converging, and every one of them creates validation seats:

- The ECL transition (the big one). The RBI's final directions of 27 April 2026 move Indian banks to expected-credit-loss provisioning from 1 April 2027 — and the directions explicitly demand governance and model-risk management around ECL estimation. Every commercial bank now needs PD/LGD/EAD-style models built and independently validated on a deadline, with a provisioning glide path running to March 2031. That is a multi-year, industry-wide wave of exactly this work.

- The RBI's direction of travel on credit models. Its draft circular "Regulatory Principles for Management of Model Risks in Credit" (5 August 2024 — still a draft, so quote it as one) proposes board-approved model policies and validation that is independent of development, done before deployment, after material changes, and at least yearly — with results reported to the board's risk committee, and the RBI free to commission external validation of any model, including vendor models.

- The global rulebook GCCs already follow. The India hubs of global banks validate to the US Federal Reserve's SR 11-7 guidance — the document that defined "effective challenge" — and to Basel-era expectations on internal models (our Basel norms explainer shows where models sit in that framework). Those hubs run large, permanent validation teams in India.

Put simply: development hiring rises and falls with projects; validation hiring is being written into regulation. Regulation-driven demand is the stable kind.

What Does a Model Validator Do All Day?

The honest day-to-day, in the order a real validation runs:

- Read the model documentation — then test whether it tells the truth. Does the described methodology match the code?

- Check the data. Was the build sample clean, representative and large enough? Were exclusions justified, or convenient?

- Challenge the assumptions. Why logistic regression and not something else? Why these variables? What was tried and rejected — and was the rejection sound?

- Replicate and backtest. Re-run the numbers independently. Compare predicted defaults against what actually happened. Compute the discrimination and stability metrics — KS and Gini for "does it rank risk correctly", PSI for "has the population drifted" (plain-words versions in our Python vs SAS guide, which is also the tooling half of this job).

- Build a challenger. A simple alternative model. If your challenger beats production, that is a finding.

- Write the verdict. A findings report — approved, approved-with-conditions, or rejected — defended in front of the developers and reported upward. Under the RBI's proposed rules, that trail reaches the board's risk committee.

Notice the mix: roughly half statistics and coding, half investigation and writing. The report is the product. People who can compute but not explain plateau early in this career; the reverse is equally true.

How it differs from model development, in one table:

| Model development (1st line) | Model validation (2nd line) | |

|---|---|---|

| Core question | "What is the best model we can build?" | "Can this model be trusted in production?" |

| Output | A working model | An evidence-backed verdict |

| Mindset | Creative, optimising | Sceptical, adversarial-but-fair |

| Rhythm | Project bursts | A planned annual cycle per model |

| Judged on | Model performance | Quality of challenge — what you caught |

Plain takeaway: developers build the case; validators cross-examine it. Same mathematics, opposite posture — pick by temperament, not by which sounds senior.

What Skills Do You Need?

Four layers, from foundation to differentiator:

- Statistics that you can defend, not just run. Regression, probability, hypothesis testing — plus the credit-risk trio of PD, LGD and EAD and the KS/Gini/PSI metric family. Validators get paid to know why a metric moved.

- Tooling. Python to build challengers and automate tests; read-level SAS because much of what you validate was built in it. The exact learning order is mapped in Python vs SAS for credit risk.

- Writing. The most underrated skill in the stack. A finding that is statistically right but badly written changes nothing. Validation reports go to committees; clarity is leverage.

- Regulation literacy. Know what SR 11-7 means by effective challenge, what the RBI's ECL directions demand of model governance, and where models sit in the Basel capital framework. A certification like the FRM packages most of this credibly — its Part 2 credit-risk and operational-risk areas map directly onto validation work.

What Does Model Validation Pay in India?

Honesty first: salary sites publish no reliable India page titled "model validation analyst" — the roles sit inside broader risk and quant families. So here is the adjacent named data, with sample sizes, from PayScale India (checked July 2026):

| Adjacent role (PayScale India) | Average base | Entry level | Top 10% | Sample |

|---|---|---|---|---|

| Risk Analyst | ₹6.3L | ₹3.9L | ₹20L | n=203 (upd. Aug 2025) |

| Credit Risk Analyst | ₹11.0L | ₹5.4L | ₹20L | n=27 — small (upd. Jan 2026) |

| Quantitative Analyst | ₹14.7L | ₹11.4L (n=8 — tiny) | ₹30L | n=21 — small (upd. Apr 2026) |

| Risk Manager | ₹14.3L | ₹6.1L | ₹30L | n=97 (upd. Aug 2025) |

Plain takeaway: validation seats price like quant-flavoured risk roles — entry in the ₹5–8L zone at banks and consultancies, more at GCC quant desks, with the ₹14L-plus band arriving at the senior-analyst-to-manager step. Treat the small-sample rows as direction, not promise, and read them alongside the fuller credit-risk salary guide.

How Do You Get In as a Fresher?

Four real doors, in rough order of fresher-accessibility:

- GCC risk programmes. The India hubs of global banks run standing model-risk-management teams and hire graduates into them directly. Quantitative degree + Python + a validated project is the profile their screens look for (QuintEdge counsellor guidance from placement conversations).

- Big 4 and risk consulting. Consultancies are staffing ECL build-and-validate engagements for the 2027 deadline — fresher-heavy teams where you see many banks' models in two years. The variety is the fastest education in the field.

- Bank model teams, then the internal move. Join a modelling or analytics team first; transfer into validation once you know the models from the inside. Developers-turned-validators are prized — they know where bodies get buried.

- NBFC ECL wave. Large NBFCs already run IndAS-style ECL provisioning models, and the RBI's 2026 bank directions are professionalising standards across the sector — validation-shaped work is spreading well beyond the big banks.

Whichever door, the portfolio artefact is the same: one scorecard you built, validated and documented yourself (the 8-week plan produces exactly this), plus fluency in the standard credit-risk interview questions. CAs and career-switchers have an extra lane too — mapped in credit-risk careers for CA + FRM profiles.

Where Does the Career Go?

The ladder is legible: validation analyst → senior analyst → validation lead → head of model risk management. Each step trades hands-on testing for scope — more model families (credit, market, fraud, and now AI/ML models), more committee time, more judgement calls on what "fit for purpose" means.

The exits are the quiet strength of the seat. Two years of validation teaches you every way models fail — which converts cleanly into model development, quant risk, stress-testing teams, regulatory advisory, or audit analytics. The reverse rotation (validator → developer → back) is common and career-accelerating.

And because the demand is written into regulation — SR 11-7 abroad, the ECL directions and the model-risk draft at home — the seat has unusual downturn resistance: banks can pause new lending products; they cannot pause annual validation cycles.

It will never be the loudest job in the building. It is the one the building cannot legally run without.

Model Validation Careers: Frequently Asked Questions

Bad validation is a checklist job; good validation is detective work. The interesting half is replication, challenger models and defending findings against smart developers who disagree with you. Teams vary — in interviews, ask how many findings the group raised last year and what happened to them. The answer tells you which kind of team it is.

Working Python is expected — you must replicate models and automate tests — but validation is not a software-engineering role. Statistics you can defend and reports you can write matter at least as much as code. A fresher with clean pandas plus scikit-learn skills and one documented scorecard project clears the technical bar at most teams.

FRM, clearly. Its syllabus — quantitative methods, credit risk, valuation models, operational risk — is the validator's daily vocabulary, while the CFA optimises for investment analysis. The strongest fresher combination we see is FRM Part 1 passed plus a Python-built, self-validated scorecard: one signals concepts, the other proves practice.

It is the standard from the US Federal Reserve's SR 11-7 guidance: validation must have the expertise, independence and organisational standing to genuinely contest a model — and force changes — not merely review it politely. If validators cannot reject a model in practice, the bank has documentation, not challenge. Expect this phrase in any serious MRM interview.

Increasingly, yes beyond banks. Large NBFCs already run ECL-style provisioning models under IndAS accounting, fintech lenders run scorecards that investors and partners expect to be independently reviewed, and the RBI's 2024 draft model-risk principles are aimed at regulated lenders broadly. Banks and GCCs remain the deepest markets, but the second ring is growing fast.

Validation tests models; audit tests processes — including the validation process itself. A validator re-runs a scorecard's numbers and challenges its assumptions; an auditor checks that validations happened on schedule, findings were tracked, and governance worked. Validation is the more quantitative seat, audit the more procedural one, and careers do cross between them.