Why Do Analysts Leave IB At All?

Investment banking is the rare job people fight to enter planning to leave. The reason is structural, not scandalous: an IB analyst stint front-loads your career with skills — modeling, valuation, deal process, working at speed — that other employers pay to acquire ready-made. Two to three years in, the learning curve flattens while the hours stay long. That is when the "exit opportunity" question gets real.

Exit opportunities simply means: the jobs that recruit specifically from IB alumni. The classic list — private equity (PE), venture capital (VC), corporate development, equity research, startups — all buy the same thing: someone already trained to read businesses and survive deadlines.

One honesty note before the map. The exits-in-two-years script is imported from Wall Street, where analyst classes are huge. India's IB pool is smaller, fund seats are fewer, and plenty of strong careers stay in banking. Treat exits as options you earn, not a schedule you owe anyone.

Where Do IB Analysts Actually Go?

Six real doors open off an IB analyst desk. Each trades something for something — read the last two columns as one unit, because every exit charges a price:

| Exit | What you do there | What improves | What you give up |

|---|---|---|---|

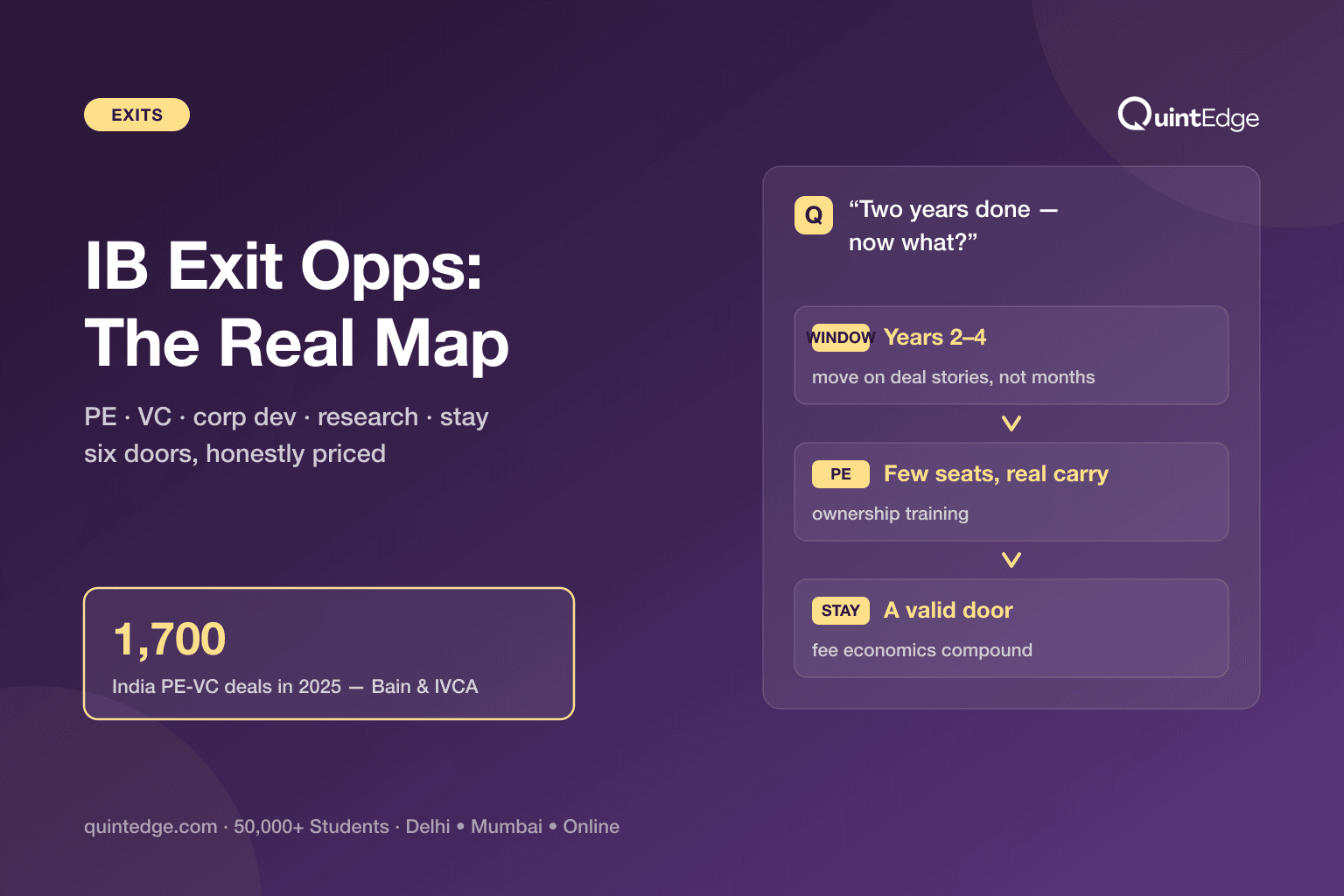

| Private equity | Buy, improve and sell companies | Ownership thinking; long-term wealth via carry | Few seats; hours stay heavy during deals |

| Venture capital | Back startups early, help them grow | Hours, variety, network; optionality | Lower cash pay early; payoffs take a decade |

| Corporate development | Run M&A inside one company | Hours and stability, one business deeply | Deal volume; the bonus curve flattens |

| Equity research | Analyse listed stocks, publish views | Public-markets craft; clearer routine | Deal adrenaline; entry pay is lower |

| Startups / founder's office | Strategy, fundraising, operations | Ownership, speed, breadth | Salary certainty; structure |

| Staying in IB | Analyst → associate → VP | Fee economics compound with seniority | The hours, for longer |

Plain takeaway: there is no strictly better exit — each door trades pay curve, hours and ownership differently, so pick by what you want more of, not by prestige.

The PE Exit: How Does It Really Work in India?

PE is the prestige exit, so it deserves the most honest treatment. The demand side is real: India's PE-VC industry invested about $36 billion across roughly 1,700 deals in 2025 (Bain & Company's India Private Equity Report 2026, with IVCA) — deal count actually rose 10% even as value fell. Funds continuously need associates who can run diligence and models without hand-holding. That associate profile is, almost by definition, a trained IB analyst.

The supply side is the catch. Fund teams are small — a large India fund might add a handful of associates a year, and boutique funds one or two. Recruiting is relationship-driven: headhunters, deal counterparties who liked your work, and referrals. The window matters too: funds want 2–4 years of deal experience — early enough to mould, senior enough to deploy.

Pay reality, from thin public data (PayScale India, checked July 2026): PE associates average ₹8.1 lakh on just 8 reported profiles, with mid-career profiles around ₹34 lakh — small samples, so treat both as rough signals. The real economics arrive later through carried interest, the team's share of fund profits, which junior staff barely touch. In cash terms, a good IB seat can out-pay a PE seat for years; you move for ownership training and the long game, not the first offer. Before targeting funds, study the landscape in our PE firms in India list, and get the full three-way comparison in IB vs PE vs VC.

What About VC, Corp Dev and the Other Doors?

Venture capital buys judgement plus network. Ex-bankers bring discipline to a business that runs on conviction; funds also hire startup operators, so the door is contested from two sides. Public pay data is nearly useless here — PayScale lists VC associates at ₹13.75 lakh on only 3 profiles — because firms are tiny and pay privately negotiated. The honest pitch for VC: better hours and enormous option value; the honest warning: cash compensation early on is often below your IB run-rate, and the carry payoff, if any, is a decade out. Scout the firms first: VC firms in India.

Corporate development — the in-house M&A team at a large company — is the quality-of-life exit. Same deal craft, saner hours, one balance sheet you know deeply. The trade: fewer deals a year and a pay curve tied to corporate bands rather than deal fees. It suits analysts who love the work but want a life around it.

Equity research converts deal skills to public markets — deep-diving listed companies and defending calls in writing. Entry pay is visibly lower (PayScale: equity analysts average ₹4.6 lakh on 32 profiles, top 10% ₹20 lakh), but senior analysts with a franchise earn strongly. If markets excite you more than deals, read what equity research actually is before deciding.

Startups and founder's-office roles pay in breadth: fundraising one week, pricing the next. Ex-IB analysts are prized for investor-facing work. Equity (ESOPs — employee stock options) replaces bonus certainty; judge the company like an investor before you join one — you have the toolkit.

When Should You Move — and When Should You Stay?

Timing beats enthusiasm. Move too early (under ~18 months) and you carry no finished deal stories; every fund interview becomes theoretical. Move too late (past ~5 years) and funds price you as a banker, not a mouldable associate — the classic window is years 2–4. Within that window, decide with four questions:

- 1. Do you have two deals you can narrate end-to-end? No → stay and finish one; exits interview on stories, not months served.

- 2. What do you want more of — ownership, hours, or breadth? Ownership → PE/VC. Hours with the same craft → corp dev or research. Breadth → startups. If the answer is "just more money soon", check your bonus trajectory first — staying may win.

- 3. Is the pull real or is the push just fatigue? Exhaustion argues for a holiday, not necessarily a new industry. Exit for something, never just from something.

- 4. Does your evidence match the door? PE wants deal execution; VC wants sector views and network; corp dev wants process ownership. Six months of targeted evidence-building beats a spray of applications.

And weigh staying honestly: banking's own ladder — analyst to associate to VP — compounds fee economics for those who stay, and India's growing deal market (1,700 deals in 2025) keeps widening the top of that funnel. The full pay curve is in our IB salary guide; the day-to-day of the senior seats is in what an investment banker does. Whichever door you choose, walk through it with evidence in hand.

IB Exit Opportunities: Frequently Asked Questions

Six real doors: private equity (the classic), venture capital, corporate development (in-house M&A), equity research, startup or founder's-office roles — and staying in IB itself, which is an underrated option with compounding pay. All six recruit for the same asset: your modeling, valuation and deal-execution training.

The standard window is 2–4 years. Under about 18 months you lack complete deal stories to interview on; past five years funds tend to price you as a senior banker rather than a trainable associate. Inside the window, readiness matters more than the clock: two deals you can narrate end-to-end is the real qualification.

Not reliably in cash, especially early. Public data is thin — PayScale India shows PE associates averaging ₹8.1 lakh on just 8 profiles versus ₹8.9 lakh for investment bankers on 51 — and a strong IB bonus year can out-pay a fund seat. PE's financial edge is carried interest, the team's share of fund profits, which becomes meaningful only at senior levels years later.

It is a deliberate trade, not a step down: the same M&A craft with saner hours and deep knowledge of one business, in exchange for fewer deals a year and corporate pay bands instead of fee-linked bonuses. For analysts who love deal work but want sustainable hours — often around major life stages — it is frequently the highest-satisfaction door on the map.

Yes, but you compete with operators, so bring investor evidence: a sector you know deeply, written deal or market notes, and a genuine startup network. Ex-IB candidates win VC seats on diligence discipline and financial rigour; they lose them by showing up with only a resume. Start publishing views and meeting founders six months before you apply.

No — it is one of the best-paying paths in Indian finance. Fee economics compound with seniority: VPs and directors who originate deals capture the industry's real upside, and India's deal count is growing (roughly 1,700 PE-VC deals in 2025, per Bain-IVCA). The exit narrative is a Wall Street import; treat staying as an active choice with its own strong economics.