How Do IB Technical Rounds Actually Work?

Technical rounds test whether you can think in financial statements and valuation under pressure. Four pillars cover almost everything asked in India: accounting links, enterprise-vs-equity value, valuation multiples and DCF, plus basic LBO and M&A logic for deal-team seats. Interviewers do not want recited definitions — they want you to walk a number through a business.

This page is a working bank of 50+ real technical questions with model answers — the technicals-only companion to our 66 IB interview questions and answers, which covers HR, fit and the broader bank. Each pillar gets two layers here: a deep walkthrough of the question interviewers escalate hardest, then a rapid-fire set you should be able to answer cold in 30 seconds each.

One rule before you start: every answer below ends at a number or a decision. Interviewers escalate until you run out of depth — the preparation goal is to run out three questions later than other candidates.

How Do the Three Financial Statements Link?

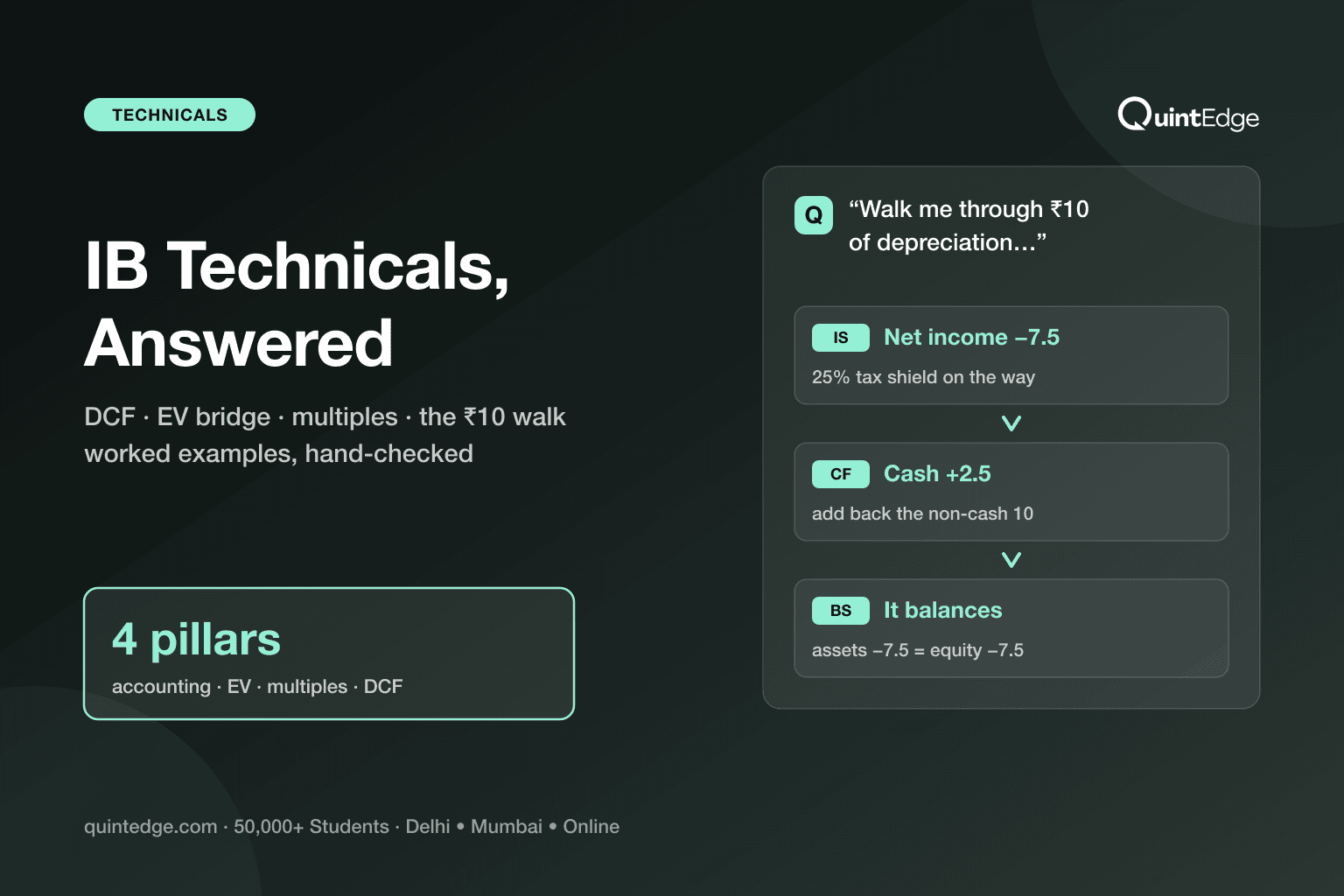

This is the opening technical in most interviews, and the follow-up is nearly always the same: "Walk me through ₹10 of extra depreciation." Depreciation is a non-cash expense — the accounting charge for machines wearing out. Learn this walk cold, with India's ~25% corporate tax rate:

- Income statement: depreciation rises ₹10, so pre-tax profit falls ₹10. Tax falls ₹2.5. Net income falls ₹7.5.

- Cash flow statement: start from net income (−7.5), add back the non-cash ₹10. Cash rises ₹2.5 — the real cash saved on tax.

- Balance sheet: assets — equipment down ₹10, cash up ₹2.5 → total assets down ₹7.5. Equity — retained earnings down ₹7.5. It balances.

All numbers illustrative, at a 25% tax rate. Notice the punchline interviewers listen for: net income fell but cash rose. Profit is an opinion shaped by accounting rules; cash is a fact — one line of that flavour shows you understand why the statements exist.

Behind this question sits the full skill of connecting the statements — if the mechanics feel shaky, build one yourself with our three-statement model guide before your interview. Ten hours of building teaches what fifty hours of reading cannot.

Accounting Rapid-Fire: 12 Questions You Must Answer Cold

These are the accounting questions Indian screeners actually open with. Answers are deliberately short — that is the skill being tested. All ₹ figures illustrative, tax at 25%.

1. Why do we need three financial statements?

Each answers a different question. The income statement: did we earn a profit this period? The cash flow statement: where did cash actually come and go? The balance sheet: what do we own and owe right now? Any one alone can mislead; together they cross-check each other.

2. If I can see only one statement to judge a company's health, which one?

The cash flow statement — companies die of cash, not of accounting losses. It is also the hardest to dress up. Then defend the choice: "but I'd reconcile it against the other two, because each alone can be gamed."

3. Walk me through a ₹20 inventory write-down.

Income statement: expense ₹20, pre-tax profit −20, tax −5, net income −15. Cash flow: start −15, add back the non-cash ₹20 → cash +5. Balance sheet: inventory −20, cash +5 → assets −15; retained earnings −15. Balances.

4. Where does buying a ₹50 machine show up?

No income-statement hit on day one. Cash flow: −50 under investing (capex). Balance sheet: cash −50, equipment +50 — assets unchanged in total. The income statement feels it later, as depreciation spread over the machine's life.

5. What is working capital, and why does growth eat cash?

Working capital = money parked in day-to-day operations: inventory + receivables − payables. A growing company buys more stock and waits on more customer payments before the sales cash arrives — so profit can rise while cash falls. That gap is why profitable retailers still borrow.

6. Why is deferred revenue a liability?

The customer paid you before you delivered — you owe them work, not money. Cash sits on the balance sheet matched by an obligation; revenue is recognised only as you deliver. Common in subscriptions and Indian ed-tech.

7. What is EBITDA and why does everyone use it?

Earnings before interest, tax, depreciation and amortisation — a rough proxy for operating cash generation that ignores financing and accounting-life choices, so firms with different debt and asset policies compare cleanly. Its flaw: it ignores capex and working capital, which are real cash costs.

8. Can a profitable company go bankrupt?

Yes — profit is recognition, cash is timing. Receivables that never convert, inventory pile-ups or a debt repayment wall can empty the bank account while the income statement still shows profit. That is why lenders watch cash conversion, not just margins.

9. What does negative shareholders' equity mean?

Liabilities exceed book assets — usually from accumulated losses, or from large buybacks and dividends that stripped equity out. It is a flag, not an automatic death sentence: some healthy companies run negative book equity after returning capital.

10. If depreciation is non-cash, why do we care about it at all?

Two reasons: it is a real economic cost (machines do wear out and need replacing), and it carries a cash benefit — the tax shield. ₹10 of depreciation saves ₹2.5 of tax at 25%. Ignore it and you overvalue asset-heavy businesses.

11. What is the difference between a prepaid and an accrued expense?

Prepaid: you paid cash before receiving the service — an asset that becomes expense over time (annual rent paid upfront). Accrued: you received the service but haven't paid — a liability (salaries owed at month-end). Opposite sides of the same timing gap.

12. How do the statements connect, in one breath?

Net income closes the income statement, opens the cash flow statement, and lands in retained earnings on the balance sheet; the cash flow statement's ending cash is the balance sheet's cash; and non-cash items reconcile the two. Practise saying exactly that sentence.

Enterprise vs Equity Value: How Do You Answer It?

Model answer in two lines: equity value is what the company's shares are worth — the owners' slice. Enterprise value (EV) is the value of the whole operating business — the price of the house, regardless of how much of it is mortgaged. The bridge between them: EV = equity value + debt − cash (plus minority interest and preferred shares in the full version).

Worked example (illustrative): market capitalisation ₹800 crore, debt ₹250 crore, cash ₹50 crore. EV = 800 + 250 − 50 = ₹1,000 crore. A buyer of the whole business takes on the ₹250 crore of debt but pockets the ₹50 crore of cash, so the business itself costs ₹1,000 crore.

Standard escalations, with the answers interviewers expect:

- "Why subtract cash?" Because cash is not needed to run operations — a buyer can use the company's own cash to offset the price.

- "Can EV be lower than equity value?" Yes — when cash exceeds debt (many Indian IT companies). Net cash makes the bridge negative.

- "Can EV be negative?" Rarely — cash exceeding market cap plus debt. It happens in deeply distressed or forgotten stocks; usually the market is saying the business burns cash.

- "Does raising debt change EV?" Not directly — debt up, cash up equally, they cancel. What changes EV is the market re-pricing the business.

EV & Equity Value Rapid-Fire: 8 Questions

1. Why do we add debt to get enterprise value?

Because a buyer of the whole business inherits its obligations. The house analogy: the true price of a house is what you pay the owner plus the home loan you take over.

2. Why add minority interest?

Consistency. If a company consolidates 100% of a subsidiary's revenue and EBITDA while owning, say, 80%, the value of the other 20% (the minority) must sit in EV too — otherwise you would divide a whole-business metric by a part-business value.

3. A company buys back ₹100 crore of shares. What happens to EV?

Roughly nothing. Equity value falls ~₹100 crore, but cash also falls ₹100 crore, and less cash means EV rises by the same amount — the two legs cancel. EV = E + D − C stays flat; only the capital structure shifted.

4. And if it pays a ₹100 crore dividend?

Same logic, same answer: equity value down, cash down, EV unchanged. Distributions move value between the company and its owners; they do not change what the operating business is worth.

5. The company issues ₹200 crore of debt and keeps it as cash. EV?

Unchanged — debt +200 and cash +200 cancel in the bridge. Say the principle: financing events alone do not move EV; operating value does.

6. How do leases fit into EV now?

Under Ind AS 116 / IFRS 16, long-term leases sit on the balance sheet as lease liabilities — debt-like obligations. Consistent practice: include lease liabilities in the bridge and use EBITDA definitions that match (a favourite trap in airline and retail comps).

7. Which is usually bigger, EV or equity value?

EV, because most companies carry more debt than cash. The exception cluster in India: cash-rich IT services and some FMCG names, where net cash pushes equity value above EV.

8. Where do convertibles go — debt or equity?

Depends on where they stand: in-the-money convertibles are treated as equity (add the shares they convert into, using the treasury or if-converted method); out-of-the-money convertibles stay as debt. State the rule, then say which applies to the company at hand.

Which Valuation Multiples Must You Know?

A multiple is just a price tag divided by a performance number — "how many rupees per rupee of earnings". The trap in interviews is mismatching the two sides. Rule: whoever the numerator belongs to, the denominator must belong to the same group. EV pairs with pre-interest numbers (EBITDA, EBIT, revenue); equity value pairs with post-interest numbers (net income, book value).

| Multiple | Pairs | Use it when | Watch out |

|---|---|---|---|

| EV / EBITDA | Whole business ÷ pre-interest cash proxy | Comparing firms with different debt levels — the workhorse | Ignores capex; bad for asset-heavy firms alone |

| EV / EBIT | Whole business ÷ operating profit | When depreciation is a real economic cost (manufacturing) | Depreciation policies differ across firms |

| P / E | Share price ÷ earnings per share | Mature, profitable firms; the market's favourite shorthand | Meaningless for loss-makers; distorted by leverage |

| EV / Revenue | Whole business ÷ sales | Loss-making or early-stage firms (startups, new-age tech) | Says nothing about profitability |

| P / B | Price ÷ book value per share | Banks and lenders, where the balance sheet IS the business | Book value can hide bad loans |

Plain takeaway: memorise five multiples and the pairing rule — most multiple questions are the pairing rule wearing a costume.

Quick check the interviewer may run: EV ₹1,000 crore and EBITDA ₹125 crore → EV/EBITDA = 8.0× (illustrative). Escalation: "8× against a peer set at 11× — cheap or justified?" The expected shape: check growth, margins and risk before calling it cheap — a discount can be deserved. That judgement layer is exactly what our comparable company analysis guide trains, including how to build the peer set honestly.

Multiples & Comps Rapid-Fire: 10 Questions

1. Why prefer EV/EBITDA over P/E when comparing companies?

P/E mixes operating performance with capital structure — two identical businesses show different P/Es if one carries debt. EV/EBITDA compares the business before financing choices, so a leveraged and an unleveraged peer line up fairly.

2. When is P/E actually the right tool?

Mature, consistently profitable companies with broadly similar leverage — and any context where per-share thinking dominates, like index and retail-investor conversations. It is the market's common language; just know what it hides.

3. The company's EBITDA is negative. Now what?

Climb the income statement until you find a positive, meaningful line — usually revenue → EV/Revenue — and add operating metrics the sector trusts (per-user, per-store, per-tonne economics). Say the principle aloud; it is what is being tested.

4. Why is EV/Revenue called a dangerous multiple?

Because it prices growth with no opinion on profitability. Two firms at 5× revenue can be a future cash machine and a future write-off. Use it as a placeholder, never a conclusion.

5. Which multiple for a bank or NBFC — and why not EV/EBITDA?

P/B and P/E. For lenders, debt is raw material, not financing — interest is the business — so EV and EBITDA lose meaning. Price-to-book works because the balance sheet effectively is the business.

6. Trailing vs forward multiples?

Trailing uses the last twelve months (fact); forward uses forecast earnings (opinion). Forward multiples look cheaper for growing firms. The comps rule is consistency: same period basis for every company in the set.

7. How do you actually pick the comp set?

Match the business model, not just the sector label: similar revenue drivers, margins, growth, size and geography. Five honest comps beat fifteen lazy ones — and be ready to defend every inclusion and exclusion.

8. Trading comps vs transaction comps?

Trading comps use listed peers' market prices — a minority, liquid benchmark. Transaction comps use prices paid in actual acquisitions, which usually run higher because buyers pay a control premium and price in synergies. Deal pricing leans on the second.

9. One stock trades at 30× P/E, its peer at 15×. Give three legitimate reasons.

Faster expected growth; higher quality of earnings (margins, returns on capital, lower cyclicality); and lower risk or better governance. If none of those hold, the premium is sentiment — which is your opening to argue mispricing.

10. A comps table says the company is worth 9× EBITDA but your DCF says 12×-equivalent. Which is right?

Neither automatically — they answer different questions. Comps price the company as the market prices peers today; the DCF prices its own cash flows under your assumptions. Investigate the gap: aggressive forecasts, or a genuinely mispriced sector? The gap IS the analysis.

How Do You Walk Through a DCF?

The DCF (discounted cash flow) question tests structure, not spreadsheet memory. A DCF says: a business is worth the cash it will generate, converted into today's money. Deliver the walkthrough as six steps, each one sentence:

- 1. Forecast free cash flow (cash from operations minus reinvestment) for 5–10 years.

- 2. Estimate the discount rate — WACC, the blended cost of the company's debt and equity money (equity cost via CAPM: risk-free rate + beta × equity risk premium; debt cost after tax).

- 3. Discount each year's cash flow to today.

- 4. Estimate terminal value — the value of all years beyond the forecast, usually FCF × (1+g) ÷ (WACC − g).

- 5. Discount the terminal value to today and add everything → enterprise value.

- 6. Subtract net debt to reach equity value; sanity-check against multiples.

Then prove it with small numbers (illustrative, ₹ crore): FCF of 100 / 110 / 121 over three years, WACC 12%, terminal growth 4%. Present values: 89.3 + 87.7 + 86.1 = 263.1. Terminal value = 121 × 1.04 ÷ (0.12 − 0.04) = 1,573; today that is 1,573 ÷ 1.12³ ≈ 1,119.6. Enterprise value ≈ ₹1,383 crore.

Now the escalation everyone should expect: "Your terminal value is 81% of the total — is that a problem?" Honest answer: it is normal for a growing company but it means the output leans hard on two assumptions (g and WACC), so you present a DCF with sensitivity tables, never as one number. Full build, formulas and the classic traps: our DCF model guide.

DCF Rapid-Fire: 12 Questions

1. Why free cash flow and not net income?

Because owners can only spend cash, and only after the business has reinvested to keep running. FCF strips accounting choices and charges for capex and working capital — the two real costs net income hides.

2. FCFF vs FCFE — and which discount rate goes with each?

FCFF is cash to all capital providers → discount at WACC → gives enterprise value. FCFE is cash to shareholders after debt flows → discount at cost of equity → gives equity value directly. Mixing them is the classic self-inflicted wound.

3. What is WACC, in one sentence?

The blended, after-tax price of the company's money — cost of equity weighted by equity's share, plus after-tax cost of debt weighted by debt's share, at market values.

4. Where does beta come from and what does it mean?

It measures how the stock moves with the market — market-linked risk. In practice you take listed peers' betas, strip their leverage (unlever), average, then re-lever at the target's capital structure. Bottom-up beta beats one noisy regression.

5. What do you use as the risk-free rate in India?

The 10-year government bond (G-Sec) yield — long-dated, liquid and in the same currency as the cash flows. Currency consistency is the point: rupee cash flows take rupee risk-free rates.

6. Why multiply the cost of debt by (1 − tax rate)?

Interest is tax-deductible, so the government effectively pays part of it. At a 25% rate, 8% pre-tax debt truly costs 6%. Equity gets no such shield — one reason debt is cheaper capital.

7. What is a defensible terminal growth rate?

At or below the economy's long-run nominal growth — a company cannot outgrow its economy forever. And structurally, g must be below WACC or the perpetuity formula breaks. Interviewers deliberately test with g ≥ WACC; catch it.

8. Perpetuity-growth vs exit-multiple terminal value?

Perpetuity growth is theoretically cleaner; an exit multiple (say, 8× year-5 EBITDA) is market-anchored. Best practice: compute one, cross-check with the other — a big gap means an assumption is off.

9. Your DCF gives a value far above the market price. What do you do?

Interrogate my own assumptions first — growth, margins, WACC, terminal value — and reconcile against comps. Only after that do I argue the market is wrong. Humility first is the expected shape of this answer.

10. What happens to value if WACC rises 1%?

Value falls — and disproportionately, because the terminal value (the largest, most distant chunk) is hit hardest by a higher discount rate. This is why rate cycles move long-duration growth stocks most.

11. When is a DCF the wrong tool?

When cash flows cannot be forecast sensibly: pre-revenue startups, deeply cyclical firms at peak or trough, and banks/insurers (capital structure IS the business — use dividend or residual-income approaches instead).

12. What is the mid-year convention?

Cash arrives through the year, not on 31 December — so you discount each year at t − 0.5 instead of t. It nudges present values up slightly and shows the interviewer you have actually built one of these.

What LBO and M&A Questions Get Asked?

For analyst seats, LBO and merger questions stay at intuition level. An LBO (leveraged buyout) is buying a company mostly with borrowed money — like buying a flat with a small down payment and a big home loan, renting it out to pay the EMIs, and profiting when you sell. The fund's returns come from paying down debt, growing profits, and selling at a better multiple. The full mechanics live in our LBO model guide.

Standard LBO questions: "What makes a good LBO target?" (steady cash flows, low existing debt, assets to borrow against, a sellable exit) and "Why does debt boost returns?" (you control the whole business while putting up only part of the price — gains concentrate on your small equity slice).

The M&A classic is accretion/dilution: does a deal raise or lower the buyer's earnings per share? For an all-cash deal, compare what the target's earnings yield against what the cash costs after tax. Illustrative: buy a target for ₹400 crore cash; it earns ₹28 crore → 7% yield. Fund it with debt at 8% pre-tax → 6% after tax at a 25% rate → cost ₹24 crore. Added earnings ₹28 crore vs added cost ₹24 crore → EPS rises: accretive. Flip the numbers and it dilutes. Escalation: "and in an all-stock deal?" — then compare the two companies' P/E ratios: a higher-P/E buyer using its "expensive" shares to buy "cheaper" earnings is usually accretive.

LBO & M&A Rapid-Fire: 10 Questions

1. Why does debt amplify a fund's returns?

The debt's claim is fixed; every rupee of value created above it belongs to the small equity slice. Control 100% of the business with 40% of the price, and gains concentrate 2.5× on your money — as do losses. Leverage is an amplifier, not a strategy.

2. Name the three sources of LBO returns.

Debt paydown (the company's own cash repays the loan), EBITDA growth (the business earns more), and multiple expansion (selling at a richer price per rupee of earnings). Good funds underwrite the first two; the third is the bonus they refuse to rely on.

3. Sketch a paper LBO.

Buy at 8× on EBITDA 100 → price 800; fund 60/40 → debt 480, equity 320. Five years later EBITDA is 140, exit at 8× → 1,120; debt paid down to 200 → equity proceeds 920. Money multiple 920 ÷ 320 ≈ 2.9× — roughly a 23–24% IRR over five years. (Illustrative, ₹ crore.)

4. What makes a good LBO target?

Predictable cash flows, modest existing debt, low capex hunger, a defensible market position, cost or efficiency levers a new owner can pull, and a believable exit route. In one line: a boring business with a fixable flaw.

5. What kills an LBO?

A cyclical downturn hitting fixed repayments, capex the model ignored, covenant breaches freezing the company, or paying a peak multiple and exiting at a trough. Leverage turns small operating misses into equity wipeouts.

6. All-stock deal: when is it accretive?

Rule of thumb: when the buyer's P/E exceeds the P/E it effectively pays for the target — expensive shares buying cheaper earnings add to EPS. Caveat the rule: synergies, financing mix and one-off costs move real answers.

7. Why do acquirers pay a premium over market price?

Control — the right to run the business, redirect its cash and capture synergies — is worth more than a passive minority share. The premium is the price of that control, which is also why transaction comps run above trading comps.

8. Revenue synergies vs cost synergies — which do bankers trust?

Cost synergies: eliminating duplicate functions is executable and measurable. Revenue synergies ("we'll cross-sell") depend on customers cooperating with a slide deck. Deal models routinely haircut revenue synergies for exactly this reason.

9. Cash deal vs stock deal — how does a buyer choose?

Cash signals confidence and is usually more accretive but strains the balance sheet; stock shares both the risk and the upside with the target's shareholders and preserves cash. Confidence in the target and the buyer's own valuation drive the mix.

10. What is goodwill and when does it appear?

The excess of purchase price over the fair value of the target's identifiable net assets — the accounting home of brand, relationships and overpayment. It sits on the buyer's balance sheet and is tested yearly for impairment; a write-down is a public admission of overpaying.

What Does the Boutique Excel Test Look Like?

Boutiques and Big 4 deal teams add a round the bulge banks mostly skip for freshers: a practical Excel test, typically 2–4 hours, sometimes take-home. It answers the only question a small team cares about — can you produce analyst output today? Expect one of three formats:

- Fix-the-model: a deliberately broken three-statement model — plugs, hardcodes, a balance sheet that doesn't tie. Your job: find and repair the breaks, then explain them.

- Build-from-brief: a one-page company summary with assumptions; build a compact three-statement model, run a DCF or comps on it, and state a value with two sensitivities.

- Analyse-and-recommend: a real annual report extract; compute the ratios that matter, flag three risks, and write a five-line recommendation.

What actually earns marks, in rough order: the balance sheet balances without a plug; assumptions sit in one labelled block (no numbers buried inside formulas); signs and units are consistent; the output page answers the question asked; and your verbal defence is honest — "I assumed X because Y; with more time I would test Z". Speed matters less than error-free structure: a smaller model that ties beats a sprawling one that doesn't.

Practice plan: build each of our free guides once — three-statement, DCF, comps — then rebuild the three-statement model from a blank sheet against a 3-hour clock. Two timed rebuilds is usually the gap between panic and comfort. Excel-specific drills live in our Excel for financial modeling guide and the 22 modeling interview questions.

Which Seven Answers Instantly Sink You?

Interviewers forgive a missed formula; they rarely forgive these. Each row is a real pattern from mock-interview rooms — and its fix:

| The sinking answer | Why it sinks you | The fix |

|---|---|---|

| Reciting a definition when asked to "walk through" something | Shows memorisation without mechanics | Always move a number through the statements, step by step |

| Forgetting the tax effect (dep walk, write-downs, interest) | The tax line is half the point of the question | State the tax rate up front: "at 25%…" |

| Pairing EV with net income (or P with EBITDA) | Breaks the numerator–denominator rule — instant flag | Say the pairing rule aloud before answering |

| A terminal growth rate above WACC (or above GDP) | Mathematically broken; economically impossible | Bound g below long-run nominal growth, always below WACC |

| "I'd just plug the difference" (balance sheet) | Plugs hide errors — the exact habit tests screen out | Find the break; a model that ties needs no plug |

| Quoting a multiple with no peer context ("8× is cheap") | Multiples mean nothing in a vacuum | "8× against peers at 11× — cheap IF growth and margins match" |

| Bluffing when you don't know | Small rooms; they will pull the thread until it snaps | "I don't know, but here's how I'd reason it" — then reason |

Plain takeaway: most rejections are not knowledge gaps — they are process fouls. Fix the seven habits and your existing knowledge scores higher.

How Should You Practise? The Question Ladder

Preparation fails when it is all reading and no reps. Climb this three-level ladder, with gates — do not move up until you pass the level below:

- Level 1 — cold answers (30 seconds each). The ten you must never fumble: link the three statements · walk through ₹10 depreciation · define EV and the bridge · why subtract cash · EV/EBITDA vs P/E · when to use EV/Revenue · the six DCF steps · what WACC is · what terminal value is · what makes a good LBO target. Gate: all ten aloud, no notes, one sitting.

- Level 2 — the rapid-fire banks. Work through this page's five banks (52 questions) aloud, shuffled, a pillar a day. Redo the four worked examples on blank paper: the depreciation walk, the EV bridge, the mini-DCF, the paper LBO. Gate: 90% of the bank answered in under 30 seconds each, and correct numbers twice in a row on all four worked examples.

- Level 3 — judgement escalations. Practise the "so what" layer with a friend firing follow-ups: is 8× cheap? is 81% terminal value a problem? which multiple for a loss-making startup? why might a DCF and comps disagree? Gate: 15 minutes of escalation without a blank.

Then rehearse delivery against your own resume — every project line is a technical question in disguise, which is why the IB resume guide insists on bullets you can defend for two minutes. And remember the wider round this bank sits inside: fit, HR and market questions are in the 66-question general guide.

IB Technical Interviews: Frequently Asked Questions

Four pillars dominate: linking the three financial statements (with the depreciation walk), the enterprise-vs-equity-value bridge, choosing and pairing valuation multiples, and the six-step DCF walkthrough. Deal-team interviews add LBO intuition and accretion/dilution logic. Boutiques often bolt on a practical Excel modeling test as a separate round.

Walk statement by statement at a stated tax rate (25%): income statement — pre-tax profit down ₹10, tax down ₹2.5, net income down ₹7.5. Cash flow — start at −7.5, add back the non-cash ₹10, cash up ₹2.5. Balance sheet — equipment −10 and cash +2.5 give assets −7.5, matching retained earnings −7.5. End with the punchline: profit fell but cash rose.

Move up the income statement until you find a positive number. With negative earnings, P/E is meaningless; if EBITDA is also negative, use EV/Revenue, plus operating metrics the sector trusts (per-user or per-store economics). Say the principle aloud in interviews: pick the highest line that is both positive and economically meaningful for that business.

At intuition level, yes — especially at boutiques and funds: what an LBO is, why debt magnifies returns, the three sources of returns, and a paper LBO with round numbers. Full modelled LBOs with debt schedules are more common for experienced-hire and PE interviews. Freshers should master the intuition, the vocabulary and one clean paper example.

For a prepared modeling student, roughly 25–40 focused hours: 10 on the four pillars with worked examples, 10 drilling this bank aloud through the question ladder, and the rest on mock escalations and resume defence. Starting from zero accounting takes materially longer — build a three-statement model first, because technicals compress dramatically once you have built the thing being discussed.

Yes — deliberately. Our 66-question guide covers the full interview: HR, fit, market awareness and a broad question bank. This page goes deep on technicals only: 50+ questions with model answers, hand-checked worked examples, the boutique Excel test and a practice ladder. Use this one to build technical depth, then the 66-question bank to rehearse the whole interview end to end.