What Counts as a Boutique Investment Bank?

A boutique investment bank is an advisory-only firm: it advises companies on mergers, acquisitions and fundraising, but does not lend money, run branches or trade with its own balance sheet. It sells brains, not capital. That single difference explains everything else about working at one — smaller teams, broader roles, and hiring that runs on skill rather than campus tags.

Think of the difference like hospitals. A bulge-bracket bank (the global giants — Goldman Sachs, Morgan Stanley, J.P. Morgan) is a multi-speciality hospital: every department, massive infrastructure. A boutique is a specialist surgical clinic: one thing, done deep, by a small senior team. Both do serious surgery; you learn differently in each.

For Indian freshers, boutiques matter for a blunt reason: the doors are reachable. Bulge front-office seats in Mumbai are few and campus-gated. Boutique analyst seats are won with a defended model portfolio, a sharp one-page resume and persistent outreach — inputs you control. This guide names 20 firms across three tiers, shows what actually differs about the work and the pay, and maps the way in — including the questions you should ask them.

Which Boutique Banks Should Be on Your List?

Here is a working directory of India's boutique landscape — 20 firms in three tiers, with what each is verifiably known for. Treat it as your starting research list, not a final ranking: boutiques open, merge and rebrand often, and deal flow shifts year to year.

Tier 1 — global elite and international boutiques with Indian desks. World-class advisory brands whose India teams work large, often cross-border mandates. Small teams, senior-heavy, very few junior seats — but they do exist, and laterals from domestic boutiques are a known route in.

| Firm | Known for |

|---|---|

| Rothschild & Co (India) | Few but very large mandates — 3 deals worth $4.3B in CY2025, 8th in India by value (Tracxn) |

| Moelis & Company (India) | Mumbai office since 2012, led by CEO Manisha Girotra — one of India's best-known bankers; global independent M&A advisory |

| Houlihan Lokey (India) | Mumbai and Gurugram teams (built on its 2021 GCA acquisition); M&A, capital raising, restructuring and valuation |

| BDA Partners | Asia-focused sell-side M&A specialist with nine offices across the US, Europe and Asia; ranked among India's active advisers in CY2025 (Tracxn) |

Tier 2 — homegrown leaders and the mid-market engine room. This is where most Indian boutique careers actually start: domestic firms running the country's steady flow of ₹100 crore–₹5,000 crore deals. The first two play at the largest deal sizes; the rest are the busy mid-market.

| Firm | Known for |

|---|---|

| Avendus Capital | The most-cited homegrown name — tech, consumer, healthcare and digital deals, cross-border M&A and PE advisory. KKR-backed since 2016; Japan's Mizuho agreed in Dec 2025 to buy majority control (~$523M), completing around July 2026 |

| Arpwood Capital | Mumbai, founded 2013; M&A, restructuring and private financing — the firm says it has worked on 5 of India's 10 largest M&A deals since inception |

| Ambit | Mid-market M&A and private-equity advisory across sectors; ranked among active India advisers in CY2025 (Tracxn) |

| Equirus Capital | M&A plus equity capital markets and structured finance |

| o3 Capital | Mid-market M&A in healthcare, manufacturing and consumer |

| MAPE Advisory | Long-standing mid-market M&A boutique |

| Veda Corporate Advisors | Chennai-rooted M&A house with a strong mid-size deal record |

| Singhi Advisors | M&A advisory with international deal networks |

| Spark Capital | Chennai-rooted investment banking across growth sectors |

| Merisis Advisors | Founded 2010; growth capital and M&A for companies from Series B onwards, across tech, consumer and services |

| IndigoEdge | Consumer and technology specialist — PE/VC raises and M&A from Series B to pre-IPO |

| Maple Capital Advisors | Delhi-based; M&A and capital raising typically in the $5–100M range, with cross-border and inbound-JV depth |

| Allegro Capital | Ranked among India's active M&A advisers in CY2025 (Tracxn) |

| NeoStrat Advisors | Ranked among India's top M&A advisers by value in CY2025 (Tracxn) |

| Dexter Capital Advisors | Corporate finance, M&A and fundraising advisory |

Tier 3 — sector specialists. Firms that own one niche so deeply that mandates come to them.

| Firm | Known for |

|---|---|

| Unitus Capital | Bengaluru-based; capital raising for impact, climate and financial-inclusion businesses |

Sources: firm websites and LinkedIn pages, Tracxn India M&A league table (CY2025), all checked July 2026; Avendus–Mizuho: Business Standard (17 Dec 2025) and Mizuho Financial Group filings — deal expected to complete by July 2026, founders Gaurav Deepak and Kaushal Aggarwal continuing to lead.

Plain takeaway: "boutique" spans three very different tiers — pick your tier first, because the entry route, the deal size and the interview all change with it.

Where do the domestic full-service banks fit? Kotak Investment Banking, JM Financial, Axis Capital and ICICI Securities run large advisory desks, but they sit inside broader financial groups with lending and broking arms — closer to Indian mini-bulges than boutiques. They belong on your application list too; see our 30 IB companies hiring in India for that full landscape, and types of investment banks for how the tiers differ structurally.

Boutique vs Big 4 vs Bulge: What Actually Differs?

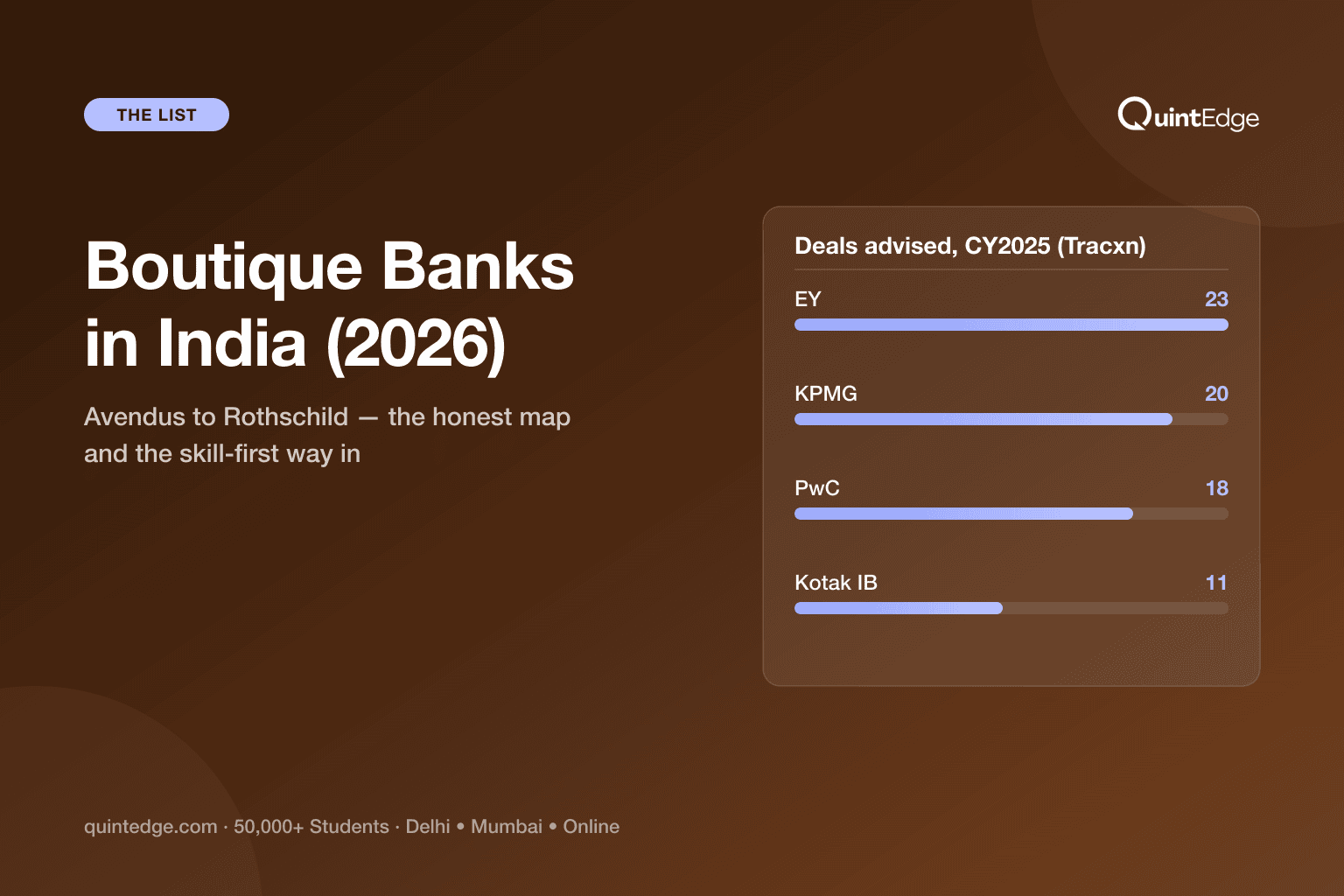

The 2025 league tables tell the real story better than prestige talk. By deal value, Morgan Stanley led India's M&A table with $16.2 billion across just 9 deals. By deal count, the busy middle dominated — EY advised 23 deals, KPMG 20, PwC 18, and Kotak 11, per Tracxn's CY2025 India M&A league table. Headlines cluster at the top; working seats cluster in the middle, where boutiques and Big 4 deal teams live.

Since most freshers actually choose between these three doors, compare all three honestly:

| Boutique | Big 4 deal team | Bulge bracket | |

|---|---|---|---|

| Your role | Generalist — model, memo, client call, all of it | Specialist within a workstream (valuation, diligence, lead advisory) | Specialist cog in a large, polished machine |

| Deal exposure | End-to-end on mid-size deals; partners in the same room | High deal COUNT — India's busiest advisers by volume | One workstream of a mega-deal at a time |

| Learning style | Steep and unstructured — you learn by owning | Structured methodology, reviews, formal training | Global process discipline, deep specialisation |

| Brand on resume | Known inside finance; explains itself less outside | Universally recognised | Opens doors globally on name alone |

| Pay | Varies widely; bonuses track deal fees | Standardised consulting-style bands | Highest, standardised analyst bands |

| Entry | Skill-based: modeling test + outreach works | Campus + off-campus rolling hiring at scale | Campus-gated internship funnel, a year ahead |

Plain takeaway: bulge buys brand, Big 4 buys volume and structure, boutique buys reps and responsibility — for learning speed per month, small usually wins.

How Does Boutique Pay Actually Work?

Boutique pay confuses students because it refuses to fit a table. The mechanics explain why. A boutique's entire revenue is success fees — typically a percentage of deal value, paid only when a deal closes. No lending income, no trading desk smoothing the year. Payroll is the main cost, so your bonus is genuinely a slice of the fees your team closed.

That structure produces three honest consequences:

- Base salaries are moderate and offers scatter. Publicly reported figures for India (PayScale, checked July 2026) put investment bankers at an average of ₹8.9 lakh across all levels, top 10% at ₹30 lakh — and boutique offers scatter around that average far more than standardised bulge bands do. Two boutiques in the same city can offer a fresher packages 2× apart.

- Bonuses swing with the deal year. One closed ₹2,000-crore mandate can fund a small firm's entire bonus pool; a dry year can shrink it to little. Ask about the last two years' deal closings before judging an offer.

- Seniority is the real payday. The economics tilt steeply toward the people who bring in mandates. That is true everywhere in banking, but at a boutique the distance between analyst pay and rainmaker pay is starker — and the path between them shorter, because titles move faster in small teams.

Illustrative example (round numbers, for intuition only): a boutique advises on a ₹800-crore sale at a 1% success fee — ₹8 crore of revenue on one deal. A six-person deal team's salaries might total ₹2–3 crore a year. One or two closings a year keeps that team healthy; four makes it a very good year. You now understand boutique bonuses better than most applicants. Our IB salary in India guide covers the full pay stack by firm type.

How Do Freshers Actually Get Into a Boutique?

Boutique hiring is refreshingly mechanical. Small teams cannot afford training benches, so they test whether you can produce analyst output now. The standard funnel has four stages — and every stage is preparable:

- 1. Get seen. Most boutique openings are never advertised. A short, deal-aware cold email with a one-page resume and a work sample beats every job portal. The exact weekly system — targets, templates, follow-up gates — is in our IB internships playbook.

- 2. Survive the resume scan. One page, numbered evidence, defended projects. Format and bullet formulas: the IB resume guide.

- 3. Pass the modeling test. Usually 2–4 hours: build or fix a three-statement model, run a quick valuation, sanity-check the output. Practise by building — start with our three-statement model guide and DCF guide. The technical questions around it are drilled in our IB technicals bank.

- 4. Defend it aloud. A partner walks your file asking "why this assumption?" — deliberately. Composure plus honest reasoning wins; bluffing dies fast in a three-person room.

Two structural notes. First, many boutique careers start as internships that convert — a 3–6-month stint is the firm's extended test drive, so treat it like one. Second, boutiques care little about college brand and a lot about evidence: for non-target students, that makes them not the fallback option but the strategy — the realistic first seat from which everything in IB (and beyond it, PE and VC) becomes reachable. Where those next doors lead: IB vs PE vs VC, compared honestly.

What Should You Ask a Boutique in the Interview?

Boutiques vary more than any other employer type in finance — which means your diligence matters more. A boutique interview always ends with "any questions for us?" Use it. These six questions separate a launchpad from a dead end, and asking them signals you think like an analyst:

- 1. "How many mandates did the team close in the last two years?" Deal flow is your learning curve AND your bonus pool. Two or fewer closings a year at a 10-person firm is a warning sign.

- 2. "Who builds the models — analysts or the VPs?" You want a firm where juniors own the file with senior review, not one where you only format decks.

- 3. "How many live deals does one analyst carry at a time?" One or two = deep reps. Four+ = you will be a coordination clerk.

- 4. "How is the bonus decided — formula, pool, or discretion?" Any honest answer is fine; a vague answer is the answer.

- 5. "Where did your last three analysts go?" Boutique alumni landing in PE funds, larger banks or strong corp-dev seats proves the seat compounds.

- 6. "Which sectors are you strongest in right now?" Sector focus decides what you will learn — a healthcare-heavy boutique makes you a healthcare-literate analyst within a year.

Plain takeaway: you are not begging for a seat; you are pricing one. Firms respect candidates who check deal flow the way investors check cash flow.

How Do You Build Your Target Shortlist?

Twenty names is a directory, not a plan. Cut it to a working list of ~15 targets (the number the cold-outreach system is built around) with three filters, applied in order:

- Filter 1 — city reality. Mumbai holds the deepest bench (Avendus, Arpwood, Ambit, Rothschild, Moelis, Houlihan Lokey and most others); Chennai has its own cluster (Veda, Spark); Bengaluru skews tech and impact (Unitus and the startup-advisory scene); Delhi-NCR has Maple and Houlihan Lokey's Gurugram team. If you cannot relocate yet, weight your list to your city — proximity makes internships and coffee meetings possible.

- Filter 2 — sector pull. Match firms to the sector you can talk about for ten minutes. Consumer/tech → Avendus, IndigoEdge, Merisis. Healthcare/manufacturing → o3 Capital. Impact/climate → Unitus. Generalist mid-market → Ambit, Equirus, MAPE, Singhi. Your outreach email improves instantly when the sector interest is real.

- Filter 3 — stage fit. Final-year student chasing a first seat → weight mid-market firms and internship-to-analyst routes. Already 1–2 years into Big 4 or a bank hub → add the global elites (Rothschild, Moelis, Houlihan Lokey, BDA), which hire far more laterally than directly.

Then run the machine: 15 firms × 2 named people, 8 researched emails a week, one work sample attached. The full weekly system with pass gates lives in the internships playbook; the resume that survives the scan is in the resume guide; the technical prep is the 50-question technicals bank.

Boutique Investment Banks: Frequently Asked Questions

An advisory-only investment bank. It advises companies on mergers, acquisitions and fundraising for a fee, but does not lend, trade or run retail banking. Teams are small and senior-heavy, so juniors work across whole deals instead of one narrow slice. Indian examples include Avendus, Arpwood, Ambit, Equirus and o3 Capital; global names with India offices include Rothschild & Co, Moelis and Houlihan Lokey.

Among homegrown firms: Avendus Capital (tech/consumer/healthcare; Mizuho agreed in Dec 2025 to buy majority control from KKR) and Arpwood Capital lead on large deals, with Ambit, Equirus, o3 Capital, MAPE, Veda, Singhi, Spark, Merisis and IndigoEdge strong in the mid-market. Among global elites in India: Rothschild & Co (8th by CY2025 deal value per Tracxn), Moelis and Houlihan Lokey. Rankings shift yearly — verify current deal flow before interviews.

Usually at entry, yes — bulge analyst bands are higher and standardised, while boutique offers vary widely with firm size and deal flow, because a boutique's whole revenue is success fees. But bonuses track closings directly, so strong deal years pay well, and titles move faster in small teams. PayScale India (July 2026) shows investment bankers averaging ₹8.9 lakh with the top 10% at ₹30 lakh — boutiques scatter across that whole range.

Take the boutique seat. Real deal reps in a small team teach more per month than waiting teaches per year, and the work compounds: two years of end-to-end boutique deals is exactly the profile larger banks and PE funds hire laterally. "Wait for bigger" only makes sense if you hold a live bulge internship offer — otherwise experience now beats brand later.

Typically 2–4 hours of practical Excel work: build or repair a three-statement model from a short brief, run a DCF or comps valuation on it, and summarise the answer in a few defensible lines. Some firms add a case discussion where a partner challenges your assumptions. They test working speed, error-checking habits and honest reasoning — not memorised definitions.

Big 4 deal teams (Deloitte, PwC, EY, KPMG) sit inside audit-and-consulting giants and were among India's busiest M&A advisers in CY2025 — EY advised 23 deals and KPMG 20, per Tracxn. They offer volume, process and brand. Boutiques offer narrower focus and deeper per-deal ownership. Both are excellent fresher entries; Big 4 suits structured learners, boutiques suit own-the-whole-thing learners.

Rarely straight from campus — their India teams are small and senior-heavy, so most junior hires are laterals with 1–3 years at domestic boutiques, Big 4 deal teams or bank analyst programmes. The practical route: build deal reps at a domestic firm first, then move. That is another reason the mid-market boutique seat is the highest-value first job in this landscape.