Why Should CA Students Learn Financial Modeling?

The CA course makes you fluent in what a company's numbers were. Financial modeling makes you fluent in what they will be. The highest-paying jobs open to a CA sit on that second skill.

A financial model is a spreadsheet that projects a company's income statement, balance sheet and cash flows forward. Someone uses it to decide: invest or not, lend or not, buy the company or not.

You already own the hardest raw material. Two years of articleship teach you how real books look from the inside. What articleship rarely teaches is building the forward view — linking three statements, projecting revenue, valuing a business. That gap is exactly what deal-side teams interview for: Big 4 transaction advisory, investment banking, equity research, FP&A.

This guide goes all the way down:

- What you will actually build in a deal team — with the spreadsheet drawn out

- The doors and their real pay floors, from ICAI's own placement rules

- The 20 questions interviewers ask CAs — with model answers

- A day-level plan that survives articleship hours

What Head Start Does a CA Student Already Have?

Non-commerce learners spend their first month of modeling just learning to read financial statements. You skip that entirely. Here is what transfers, item by item:

| What CA gave you | Where it shows up in modeling |

|---|---|

| Accounting Standards / Ind AS depth | You know why a line item moves — depreciation methods, revenue recognition, lease capitalisation — so your model assumptions are defensible, not decorative |

| Schedule III statement formats | You can map any Indian annual report into a model template quickly, because you already know where everything lives |

| Articleship audit work | You have seen real messy trial balances — so a company's actuals do not intimidate you the way they do a fresher who has only seen textbook numbers |

| Tax knowledge | Effective-tax-rate assumptions, deferred tax in projections, and the tax line of a DCF stop being a black box |

| Financial management paper | Time value of money, cost of capital and leverage — the theory behind the DCF — is already in your syllabus |

Mapped paper-by-paper, the overlap is even more concrete. The right column is what a typical FM syllabus spends weeks on. For you, those weeks are revision plus Excel craft:

| CA material you have done | FM module it pre-loads | What is genuinely new for you |

|---|---|---|

| Accounting + Advanced Accounting (Inter) | Statement structure, linking logic of the 3-statement model | Building the links keyboard-first, error-proofing, presentation standards |

| Financial Management (Inter) | Time value of money, WACC, leverage — the DCF's engine room | Choosing defensible assumptions for a real company, terminal value judgment |

| Taxation (Inter/Final) | The tax line, deferred tax in projections | When to model the book-tax gap vs hold an effective rate |

| Auditing (Inter/Final) | Scepticism — smelling a wrong number | Turning findings into EBITDA adjustments a buyer will pay against |

| SPOM Set B — Strategic Cost & Performance Management | Driver thinking: what actually moves revenue and margins | Encoding drivers as clean, switchable model inputs |

Plain takeaway: a CA student starts modeling roughly a month ahead of a typical fresher. The theory is largely revision; the craft — Excel architecture, judgment, presentation — is the genuinely new part.

What Does Articleship Teach — and What Does It Miss?

Be honest about both columns, because interviewers are.

What articleship gives you:

- Working inside completed books — vouching, ledger scrutiny, tax computations, closing entries

- Watching managements defend numbers under question (statutory-audit articles especially)

- The instinct for when a number smells wrong — priceless when you must judge a growth assumption later

What it usually does not give you:

- Building a linked 3-statement model from a blank sheet

- Projecting revenue drivers and choosing a discount rate

- Running scenarios and presenting a valuation to someone betting money on it

Some students in larger firms touch this in due-diligence support work. Most only see it from the audit side — checking a model someone else built, if at all.

One trap to avoid: assuming Excel comfort equals modeling skill. Articleship Excel is filters, pivots and reconciliations. Deal-desk Excel is keyboard-driven model architecture. Different muscle, same gym.

When in the CA Journey Should You Learn Modeling?

Under ICAI's New Scheme (in force since 1 July 2023): articleship is two years, it begins after both Intermediate groups plus ICITSS, and training must end at least six months before your Final exam month (ICAI New Scheme FAQs, checked in July 2026). That mandated gap is the study window.

This calendar creates three realistic windows to learn modeling — and one window to avoid:

| Window | Fits you if… | Watch out for |

|---|---|---|

| Window A — Articleship year 1–2, evenings/weekends | Your firm hours are predictable; you want deal-team exposure during training (some firms move strong articles toward DD/TAS work) | Busy season — pause the course calendar in January–March and September, not your sleep |

| Window B — The post-articleship Final-prep gap | You can spare 4–6 focused hours a week without touching Final study blocks | Final comes first. If mocks slip, modeling waits — a certificate is retakeable; an attempt is expensive |

| Window C — Right after Final results | You want to enter placements with a portfolio of models, not just a marksheet | The 8–12 weeks before campus placements are the highest-leverage stretch — do not idle them |

| Avoid — The month before any exam attempt | Nobody | Split attention degrades both. Exams win, always |

Plain takeaway: the best windows are articleship evenings (if your hours allow) and the sprint right after Final results. Never trade exam-prep hours for modeling hours.

What Will You Actually Build in a Deal Team?

"Financial modeling" sounds abstract until you see the files. For a CA, the fastest door is Big 4 or mid-firm transaction services. Its signature file is the QoE — quality of earnings — analysis, inside a due-diligence databook (the workbook of checks a buyer's advisors build before a deal).

QoE answers the one question a buyer cares about most: of the profit this company reports, how much is repeatable?

The method is pure CA-plus-model thinking:

- Start from reported EBITDA — profit from running the business, before interest, tax, depreciation and amortisation. The deal world's favourite profit line.

- Adjust, item by item, for things that will not repeat under a new owner — the promoter paying himself above market, a one-time subsidy, a lucky forex gain.

- Attach evidence to every line — an invoice, a ledger, a contract. Exactly the muscle articleship built.

Here is the tab, drawn out:

Around that QoE tab, a full databook adds three more analyses:

- Working capital — how much cash the business eats month-to-month; it sets the "peg" (explained in the question bank below)

- Net debt — everything debt-like beyond loans: lease liabilities, unpaid dividends, disputed dues

- Revenue quality — customer concentration, March-quarter spikes, related-party sales

On the IB side, the same skills produce the 3-statement model, DCF and comps deck. Every file leans on the judgment you already practise: is this number real, and will it repeat?

Plain takeaway: deal teams do not pay CAs to re-audit. They pay them to convert audit-grade scepticism into adjustments and models that move prices by crores.

Which Doors Open for a CA Who Can Model — and at What Pay?

Start with the credential's own floor, because ICAI publishes one. In its campus placement drives, ICAI sets minimum pay slabs recruiters must offer to get the best interview slots. The 64th-round rules (April–May 2026, largest centres; ICAI 64th campus brochure, checked in July 2026):

| Interview slot a recruiter wants | Minimum domestic CTC ICAI requires |

|---|---|

| Day Premier (first pick of candidates) | ₹20 lakh+ (or US$50,000+ international) |

| Day 1 | ₹14 lakh+ |

| Day 2 | ₹12 lakh+ |

| Day 3 | ₹11 lakh+ |

| Day 4 | ₹10 lakh+ |

| Mid-tier centres | ₹9 lakh+ |

| Smallest centres (Bhopal, Lucknow, Patna, etc.) | ₹7.2 lakh+ |

Plain takeaway: a recruiter who wants first pick of fresh CAs must offer at least ₹20 lakh. The pay slabs are a published rulebook, not a rumour.

The outcomes around those floors (all ICAI, checked in July 2026):

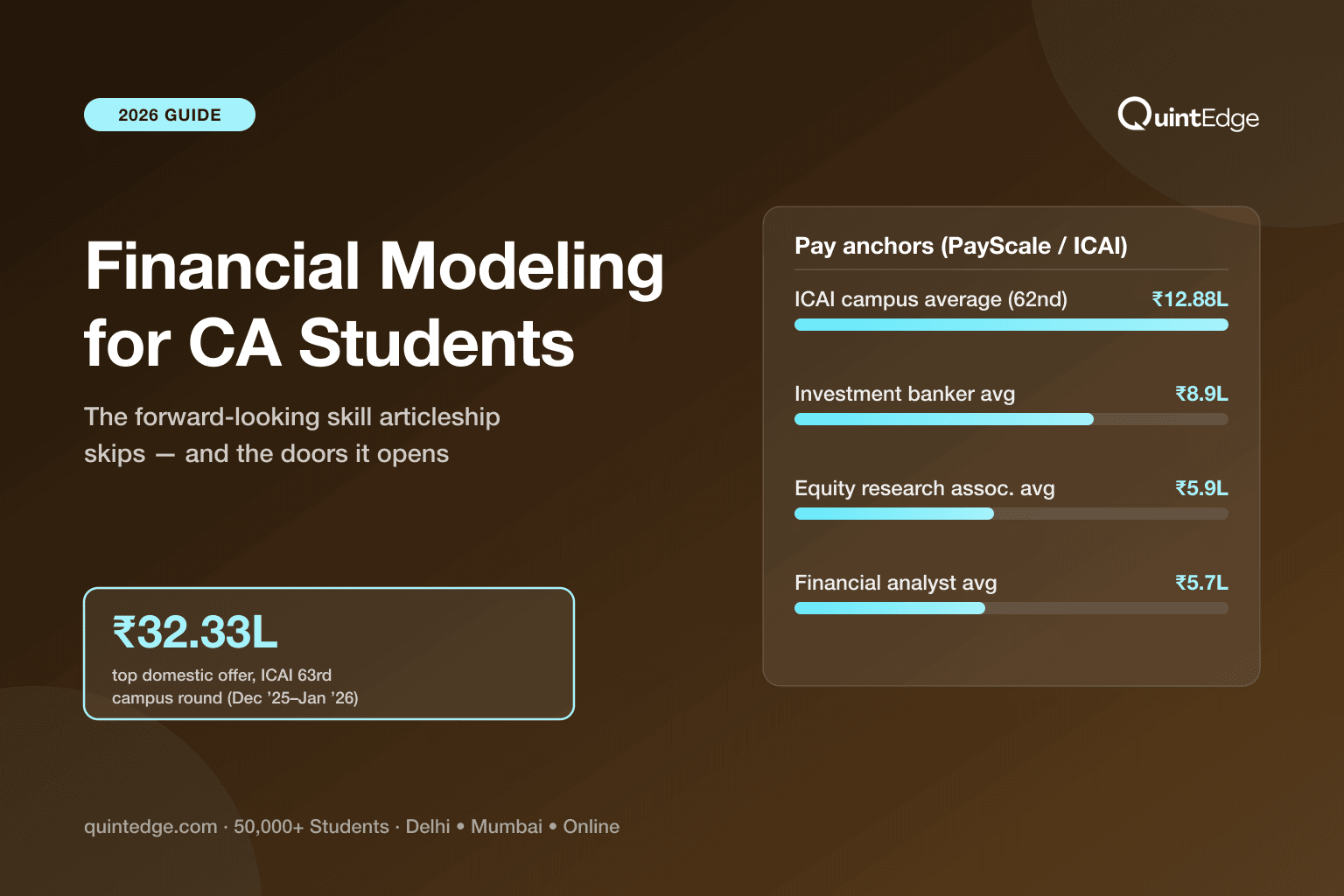

- 62nd round (Aug–Sep 2025): 157 organisations · 3,795 offers · 2,931 accepted · ICAI-reported average ₹12.88 lakh · top domestic offer ₹26.60 lakh (Power Finance Corporation)

- 63rd round (Dec 2025–Jan 2026): 145 organisations · 2,480 offers · 1,892 accepted · top domestic offer up to ₹32.33 lakh · ICAI published no average for this round — distrust anyone quoting one

- Who recruited in the 63rd: all four Big 4 networks' India entities, Nomura Services India, D.E. Shaw India, DBS, ICICI Bank, Axis Bank, IDFC FIRST Bank, Bajaj Finserv, BSE, NSE, Reliance Industries, EXIM Bank, SIDBI, Grant Thornton Bharat, MSKA & Associates

Now the doors themselves, with what modeling adds at each:

Door 1 — Big 4 transaction services / deal advisory. The QoE work drawn above. For articles already inside Big 4 or mid-size firms, demonstrated modeling often moves you from audit staffing to deal staffing — without changing employers. The highest-probability first deal seat for a CA.

Door 2 — Investment banking. Model assembly under deadline: pitch decks, DCFs, comps. CAs enter via Big 4 TAS, boutiques, or directly — the route map is in the IB career guide. PayScale India: ₹8.86 lakh average, top 10% near ₹30 lakh (n=51, updated 26 Mar 2026; checked in July 2026).

Door 3 — Equity research. Forecast quarters, build earnings models, write a view. Your Ind AS depth becomes an edge when companies massage numbers — see what equity research is. PayScale: research associates ₹5.92 lakh average, entry ₹4.15 lakh (n=41, updated 18 Apr 2026).

Door 4 — FP&A / corporate finance. Budgets, forecasts and variance stories for the CFO. Calmer hours, real modeling daily, and the ladder where the CA badge compounds — toward controller and CFO seats. PayScale's financial-analyst page (the largest sample here): ₹5.70 lakh average, entry ₹3.88 lakh (n=1,102, updated 25 May 2026).

Door 5 — Credit and lending desks. Project borrower cash flows before the bank lends. PayScale: credit analysts ₹8.13 lakh average, jumping to ₹8.21 lakh within 1–4 years (n=122, updated 27 May 2026). With statistics added later, this bridges into the credit-risk modeling track.

Want the full six-lane comparison — a realistic Tuesday in each, switching costs, a 90-day break-in plan? That is the companion piece: financial modeling career paths. Weighing a second credential instead? Compare CFA after CA and FRM after CA — modeling is faster than both, and stacks with either.

What Should You Learn First — and in What Order?

Follow the ladder deal teams themselves climb. Each rung reuses the previous one — and for a CA, the first rung is mostly revision:

- Rung 0 — deal-desk Excel. Keyboard-first navigation, clean formatting, error-proofing: the Excel guide

- Rung 1 — the 3-statement model. One company; income statement, balance sheet and cash flow linked, so a ₹1 change anywhere flows everywhere. Your Ind AS knowledge makes this fast — build along with the 3-statement guide

- Rung 2 — the DCF. Project free cash flows, choose a discount rate, add a terminal value. Your FM paper covered the theory; the craft is assumption judgment — the DCF guide walks a full Indian example

- Rung 3 — comps. Value a company against similar listed ones. Fast, market-anchored, and the first thing juniors update — the comps guide

- Rung 4 — the LBO. Private-equity math: buy with borrowed money, grow, repay, exit. Optional for FP&A, required for PE-facing roles — the LBO guide

The 20 Questions Deal-Side Interviewers Ask CAs — With Model Answers

Interviewers calibrate to your background. A CA gets fewer "what is EBITDA" softballs and more "you audited this — now price it" probes. These twenty come up constantly across TAS, IB and FP&A rounds.

The answers are deliberately short. Say this much confidently, then let them dig.

Set A — accounting-to-model bridges. They assume you know the accounting; they test the linkage.

1. "Walk me from net profit to free cash flow."

Start with net profit. Add back non-cash items — depreciation, amortisation. Adjust for working-capital moves (more receivables = less cash). Subtract capex. Close with the line they want to hear: profit is an opinion shaped by accounting policy; cash is a fact — the model prices the fact.

2. "Depreciation rises ₹10 (tax 25%). Take me through the three statements."

P&L: EBIT falls 10, tax falls 2.5, net profit falls 7.5. Cash flow: start at −7.5, add back the non-cash 10 — cash rises 2.5. Balance sheet: PP&E −10 and cash +2.5 on the asset side (net −7.5); retained earnings −7.5 on the other. Both sides tie. Practise until this takes 30 seconds.

3. "Why can EBITDA grow while cash shrinks?"

EBITDA ignores three cash realities: working capital soaking up money as the business grows, capex, and interest-plus-tax. A company can book profits into receivables it never collects. That is why lenders and buyers stare at cash conversion, not just EBITDA.

4. "Where does Ind AS 116 bite when you compare EV/EBITDA across companies?"

Capitalised leases push rent out of operating costs, so EBITDA rises — while lease liabilities join debt. Compare a company on Ind AS 116 with one on old-style operating leases and both the top and bottom of the multiple are distorted. Fix: consistent treatment across the peer set, and say which convention you chose.

5. "How do you treat deferred tax in projections?"

Two honest options. Model the book-tax depreciation gap explicitly if it is big and forecastable. Or hold a justified effective tax rate and state the assumption. The wrong answer: letting the deferred-tax balance drift forever with no reason.

6. "Is negative working capital good or bad?"

Depends on why. Customer advances funding the business — many retailers — is strength: customers finance your growth. Stretched unpaid suppliers is a warning: borrowed time, not efficiency. Same number, opposite stories. Check which one the ledgers tell.

7. "A provision written back boosted this year's profit. QoE treatment?"

Adjust it out. A write-back is yesterday's over-caution reversing — not a repeatable earning. And flag the original over-provisioning too: it shows management's provisioning habits cut both ways.

Set B — valuation judgment. Where fresher answers separate from CA answers.

8. "Your DCF says ₹500 crore; comps say ₹300 crore. Which is wrong?"

Neither, until audited. Check the DCF first: how much value sits in the terminal number, the growth-vs-WACC gap, the margin path. Then the comps: do the peers actually match the target's growth and returns? Usually the DCF carries the optimistic assumption. Say you would reconcile the gap — never average it.

9. "Terminal value is 80% of your DCF. Problem?"

Common, but worth stress-testing — it means the price rests mostly on the far future. Sanity-check the implied exit multiple. Extend the forecast if the business is still ramping. Show the sensitivity. Never hide the 80% — disclose it and defend it.

10. "Why can't terminal growth equal or exceed the discount rate?"

The forever-growth formula divides by (WACC − g). As g approaches WACC, you divide by zero — value explodes to infinity, which is nonsense. No company outgrows its discount rate forever. Cap g near long-run nominal GDP growth.

11. "The company is loss-making. Which valuation methods survive?"

Three survive: multiples on revenue or gross profit (against same-stage peers), a DCF built on an explicit path to profit (state when and why margins turn), and asset or replacement-cost views as floors. EV/EBITDA dies when EBITDA is negative — say so before they ask.

12. "Your model has circular references — interest needs debt, debt needs cash, cash needs interest. Handle it."

Three accepted routes: compute interest on opening balances (breaks the loop, slightly conservative); switch on Excel's iterative calculation, knowingly; or a copy-paste breaker in bank-grade models. What matters is choosing deliberately — and saying why.

13. "Why is EV/EBITDA meaningless for a bank?"

For a bank, debt is not financing — it is raw material. Interest is the cost of goods. Enterprise-value maths collapses. Banks are valued on P/E and P/B against return on equity — which is why bank models project loan books and margins, not EBITDA.

14. "Promoter pays himself ₹5 crore above market; reported EBITDA is ₹20 crore; the deal prices at 8× EV/EBITDA. Impact?"

Adjust the salary to market: EBITDA becomes ₹25 crore. At 8×, value moves from ₹160 crore to ₹200 crore. One payroll ledger line moved the price ₹40 crore. This is the QoE tab from earlier, priced (numbers illustrative).

Set C — due-diligence scenarios. Your articleship, weaponised.

15. "Revenue spikes every March. First three checks?"

One: April–May credit notes and sales returns — stuffed sales reverse. Two: March receivables ageing versus the year's pattern. Three: dispatch and e-way-bill evidence behind year-end invoices. You are testing whether Q4 sales are real demand or next quarter's sales pulled early.

16. "Receivables red flags in a due-diligence?"

Ageing drifting longer. A few buyers holding most of the balance. Related-party receivables growing faster than related-party sales. Receivable days far above peers. Post-year collections not matching the ledger. Any two together change the working-capital peg — and maybe revenue quality itself.

17. "What goes into net debt beyond bank loans?"

Lease liabilities. Declared but unpaid dividends. Disputed statutory dues likely to become payable. Redeemable preference capital. Restricted cash that is not really free. The buyer's rule: anything that behaves like debt gets priced like debt — and every line shifts the equity value rupee-for-rupee.

18. "Name adjustments you would test beyond the obvious one-offs."

Under-market rent on promoter premises — a buyer will pay full rent. Costs capitalised that peers expense. Provisions timed to flatter a year. COVID-era subsidies still sitting in the base. Forex or asset-sale gains hiding inside "other income". Each needs a ledger trail, not a hunch.

19. "Explain the working-capital peg in plain words."

Buyer and seller agree what a normal level of working capital is — say ₹30 crore, from a 12-month average. Deliver the business with ₹26 crore and the price drops ₹4 crore, rupee-for-rupee. Deliver more and it rises. The peg stops the seller from quietly draining the till between signing and closing.

20. "Which audit finding changes a valuation most?"

Anything touching revenue recognition timing — because it flows straight into EBITDA and gets multiplied. A ₹2 crore cut-off correction at 8× is ₹16 crore of price. Provisions and impairments matter; multiples make revenue-line findings the expensive ones.

Drill these against the wider sets — FM interview questions for the general bank, and the 50-question IB technical bank before a deal-side round. Pass standard: every answer above, aloud, without notes, under a minute each.

A 6-Week Plan That Survives Articleship Hours

This grid assumes Window A: you are in articleship, giving 6 focused hours a week — Tuesday, Wednesday and Thursday evenings (1 hour each, 9:30–10:30 pm) plus one 3-hour Saturday block. Total ≈ 36 hours to a presentable two-model portfolio.

In Window C (the post-results sprint), run each week in 2–3 days instead.

| Week | Tue (1h) | Wed (1h) | Thu (1h) | Sat (3h) | Pass gate before next week |

|---|---|---|---|---|---|

| 1 — Excel re-training | Keyboard navigation drills — no mouse for 30 min | Formatting conventions: inputs blue, formulas black, one style sheet | Rebuild a simple P&L layout from memory | Error-proofing: named ranges, IFERROR discipline, checks row; rebuild the P&L in under 20 min | A clean P&L skeleton built keyboard-only, twice, without looking anything up |

| 2 — Statements in | Pick your company (a NIFTY name whose sector you audited a peer of); download 2 annual reports | Map the P&L into your template — actuals for 3 years | Map the balance sheet; park anything odd in a questions list | Cash flow + full linkage: change any actual, everything flows | Three years of actuals in, statements linked, zero hardcoded subtotals |

| 3 — Projections | Revenue drivers: volume × price or segment growth — one-line justification each | Cost lines: fixed vs variable split, margin logic | Working capital: receivable days, inventory days, payable days from history | Debt schedule + full 5-year projection; balance the balance sheet with no plugs | The gate: balance sheet balances every projected year — if it plugs, week 4 waits |

| 4 — DCF | Free-cash-flow bridge from your projections | WACC: build it, then say each input's justification aloud | Terminal value both ways: forever-growth and exit multiple — reconcile them | Sensitivity table (growth × WACC) + one-page valuation summary | You can defend every assumption in two sentences; you know the terminal value's share of total value |

| 5 — Comps | Pick 5 peers; justify each inclusion in one line | Spread multiples: EV/EBITDA, P/E — consistent Ind AS 116 treatment (question 4!) | Outlier check: why is the cheapest peer cheap? | Comps summary page; compare vs your DCF — explain any gap in writing | Comps median within a sane range of the DCF, and the gap has a written reason |

| 6 — Polish + rehearse | Format both models to hand-over standard | Write the 2-sentence story of each model | Run the 20-question bank above, aloud | Full mock: a friend (ideally a non-CA) follows your 10-minute model tour; fix what confused them | Tour lands in 10 minutes; question bank cleared without notes |

Two standing rules:

- Fall-behind rule: if a week slips, push everything back a week. Never compress the next week, never skip a gate. A balanced model a week late beats a broken model on time.

- Busy-season rule: in January–March and September, pre-emptively halve the plan (drop Tue/Thu) and accept twelve weeks instead of six.

Plain takeaway: six weeks at six honest hours turns a CA student into someone with a defensible two-model portfolio — the file deal-side interviewers actually ask to see.

What Your Portfolio Files Must Contain

"I know financial modeling" is a claim; a file is proof. Walk into interviews — or attach to cold emails — exactly two workbooks, built to this spec:

| File | Sheets, in order | The one thing reviewers check first |

|---|---|---|

| Workbook 1 — Operating model + DCF (your Week 2–4 build) | Cover & read-me → Assumptions (all inputs, blue) → P&L → Balance sheet → Cash flow → Debt schedule → DCF → Sensitivities → Checks | The checks sheet: does the balance sheet tie in every year, with a visible zero-error flag? |

| Workbook 2 — Comps set (Week 5) | Cover → Peer selection logic → Input sheets (one per peer) → Multiples spread → Output summary with the DCF comparison note | Peer logic: can you defend why each of the five belongs — plus the Ind AS 116 consistency note |

Three presentation rules that signal "trained, not YouTubed":

- Every input cell blue, every formula cell black — consistently

- A read-me sheet that lets a stranger navigate without you

- No hidden sheets — hiding your workings reads as hiding your errors

Add a one-page PDF summary of each workbook, for recruiters who will not open Excel on a phone.

Plain takeaway: two clean workbooks with a checks sheet and a read-me beat ten half-finished templates. Reviewers open the checks sheet first — build for that moment.

Does a CA Even Need a Course for This?

Honest answer: you can self-learn from free material, and disciplined people do. A structured programme buys three things self-study struggles with:

- A reviewed portfolio — someone senior tears your model apart before an interviewer does (the Week-6 mock, done professionally)

- Placement leverage — a course with hiring relationships converts skill into interviews

- Speed — a syllabus prevents the three-month YouTube wander

Price that against your Window C weeks. The 8–12 weeks before placements are the most expensive weeks of your CA life to waste.

Whichever route you choose, the sequencing advice stands: exams first, modeling in the gaps, portfolio before placements. Fee context, if you want it: the FM course fees guide.

Financial Modeling for CA Students: Frequently Asked Questions

Yes, if your firm's hours are predictable. Six focused hours a week — three weekday evenings plus one Saturday block, exactly as the grid above lays out — completes a two-model portfolio in about six weeks. Pause during busy season (typically January–March and September). Never study modeling in an exam month; exam preparation always outranks the course calendar.

More than you would expect. Auditors increasingly review management's impairment models, expected-credit-loss workings and going-concern projections. An auditor who can rebuild the model finds the weak assumption faster than one who can only read it. It also keeps the deal-advisory door open inside your firm — without changing employers.

Modeling first, in most cases. It takes weeks rather than years, produces interview files immediately, and stacks under a later CFA if research calls you. Choose CFA first only if you are certain about investment management and can commit to multi-year exam cycles right after Final. The full comparison: CFA after CA and FM vs CFA.

Often, yes — especially Big 4 TAS and boutique IB rounds. Expect a timed databook exercise, a broken model to fix, or a rapid three-statement build. That is why the plan above spends week 1 purely on keyboard-first Excel, and why your portfolio needs a checks sheet — reviewers open it first. The question bank covers the spoken layer; the live layer is speed plus error-proofing, which only practice builds.

No database isolates "CA + modeling", so distrust precise premiums. The named data: ICAI's 62nd round averaged ₹12.88 lakh; the 63rd's top offer hit ₹32.33 lakh; and day-slot rules force ₹20 lakh+ offers from recruiters wanting first pick. Deal-side roles carry the widest top-end ranges on PayScale. The honest claim is which doors open — not a guaranteed markup. Numbers by role: the FM salary guide.

Indirectly. Building DCFs makes the valuation and financial-management portions feel concrete rather than formulaic, and statement-linking sharpens your speed on accounts problems. But do not learn modeling for Final. The syllabus overlap is a bonus, not the point — and course hours must never displace exam-prep hours.

Often it is the highest-return move available. Your Inter-level accounting plus articleship experience is real, marketable raw material. Modeling converts it into a portfolio that FP&A, valuation-support and mid-market advisory teams hire on demonstrated skill — not the membership certificate. Many readers in this position also weigh the broader after-CA options map.