What Careers Open Up After Financial Modeling?

Learning financial modeling — building linked projections and valuations of real companies in Excel — opens six career lanes in India:

- Investment banking (IB) — helping companies do deals

- Equity research — forecasting listed companies and publishing a view

- FP&A (financial planning & analysis) — being the modeler inside a company

- Private equity & venture capital (PE/VC) — investing in companies

- Credit desks — deciding bank loans

- Big 4 transaction advisory — checking companies before deals

All six interview you on the same three files: a 3-statement model, a DCF and a comps set. (A DCF values a company from its future cash; comps value it against similar listed companies.)

Then the lanes split — sharply. Different pace, different pay shape, different daily life. An IB analyst and an FP&A analyst may build near-identical spreadsheets in year one, while living completely different weeks.

This guide gives each lane the full file: the actual work, a realistic Tuesday, entry doors ranked, the pay ladder with named sources, the interview test, and where people go two years later. New to the skill itself? Start with what financial modeling is and come back.

How Should You Read the Salary Numbers Below?

Every salary figure in this post comes from a named source, with its sample size shown. Salary content in India is full of invented numbers — these three rules keep you safe:

- Averages hide shape. "Average ₹8.9 lakh" can mean most people near ₹8.9 lakh — or many at ₹4 lakh and a few at ₹30 lakh. So we show the top-10% figure beside the average wherever the source gives it.

- Sample size decides trust. A number from 1,102 profiles beats a number from 8. Anything under 30 profiles is marked small; under 10 is tiny. Treat tiny samples as stories, not statistics.

- Base salary is not total pay. PayScale figures are annual base salary unless stated. Bonuses in deal-side jobs sit on top — read these numbers as the floor of the picture.

Plain takeaway: trust big samples, read ranges not averages, and remember bonuses come extra. Full role-by-role tables live in the FM salary guide.

Every Lane on One Screen

The reference table first, details after. All figures are PayScale India annual base salary, checked in July 2026. "Grows into" names the seat this lane's survivors typically hold at years 5–10.

| Lane | Entry (<1 yr) | Average | Top 10% | Sample | Grows into |

|---|---|---|---|---|---|

| Investment banking | ₹6.07L | ₹8.86L | ₹30L | n=51, upd Mar 2026 | VP / PE associate |

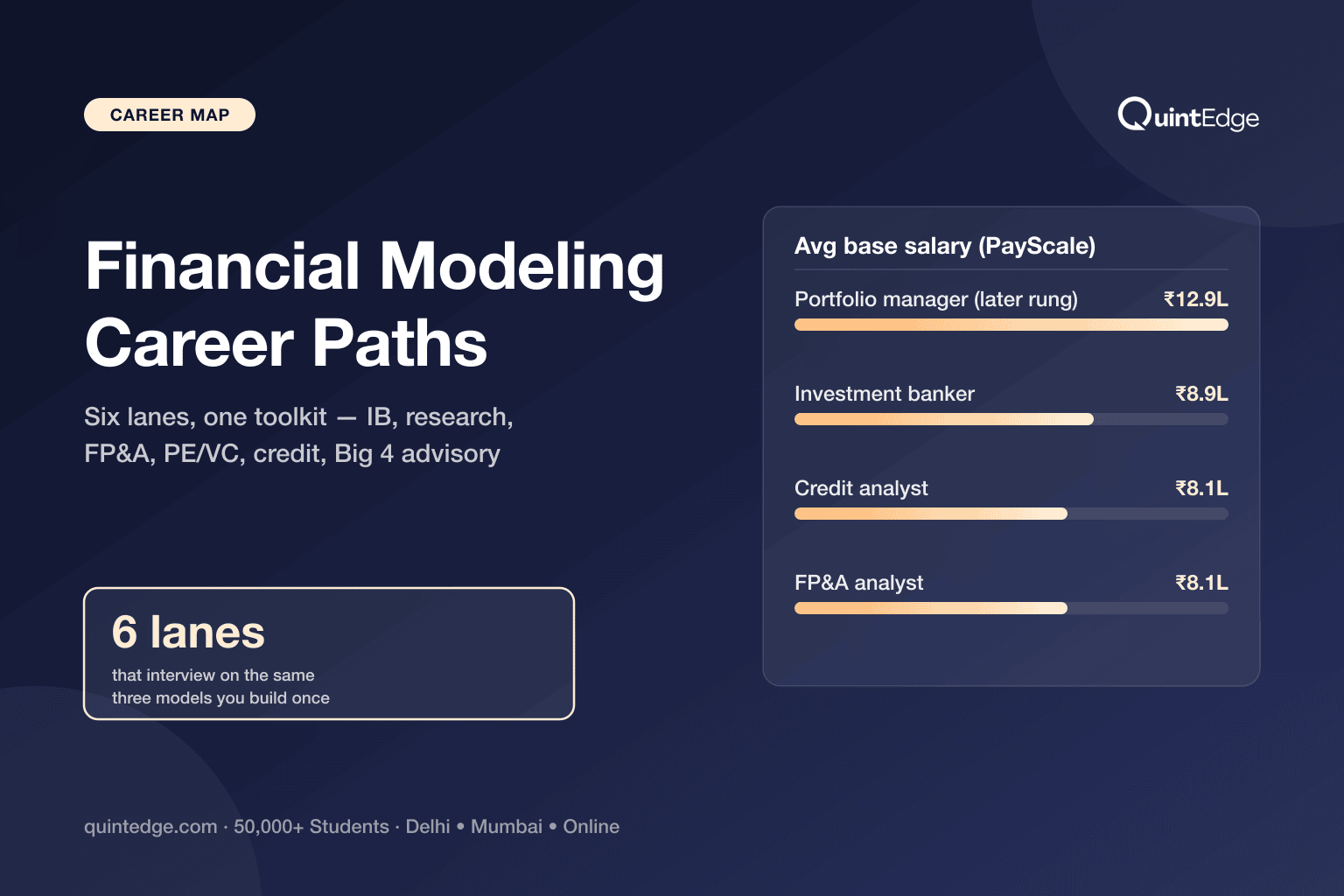

| Equity research (associate) | ₹4.15L | ₹5.92L | ₹10L | n=41, upd Apr 2026 | Portfolio manager: ₹12.9L avg, top 10% ₹40L (n=57) |

| FP&A (financial planning analyst) | ₹5.00L | ₹8.08L | ₹10L | n=32 — small | Controller: ₹19.8L avg, top 10% ₹40L (n=313) |

| PE / VC (associate) | — | ₹8.10L | — | n=8 — tiny, Jan 2025 | Mid-career PE: ₹34L total comp (5–9 yrs, tiny sample) |

| Credit desks (credit analyst) | ₹4.14L | ₹8.13L | ₹20L | n=122, upd May 2026 | Risk manager: ₹14.3L avg, top 10% ₹30L (n=97) |

| Big 4 advisory (via financial analyst data) | ₹3.88L | ₹5.70L | ₹10L | n=1,102, upd May 2026 | Manager → IB/PE lateral, or CFO track: ₹37.6L avg (n=272) |

Plain takeaway: entry pay sits within ~₹3 lakh across lanes. The real separation is in the "grows into" column — FP&A's ladder ends at controller and CFO seats (₹19.8L and ₹37.6L averages), while deal lanes stretch through bonuses and fund profits instead.

Path 1 — Investment Banking: Deals at Deadline Speed

The work. IB analysts help companies raise money or buy and sell each other. You produce four things on repeat:

- Pitch decks — slide packs arguing why a client should do a deal

- Comps sets — what similar companies are worth

- Operating models with DCFs — what this company is worth

- Deal documents — company profiles, buyer lists, data-room folders

The spreadsheet is never the end product. It feeds a ₹500-crore decision — usually due tomorrow morning.

A realistic Tuesday, year one:

- 9:30 am — fix the comments your boss left on the comps at 1 am

- 12 pm — client released quarterly results; half your model's inputs move

- 3 pm — your profit bridge will not tie; a senior helps you find why

- 6 pm — new assignment lands: a pitch for Thursday

- 11 pm — the deck is "final v7"; dinner was at the desk

That is a normal Tuesday, not a bad one. The honest hours-and-pay picture is in the IB salary guide.

Entry doors, ranked by how open they are:

| Door | How open | What gets you through |

|---|---|---|

| Boutiques (smaller specialist deal firms) | Widest for freshers — they hire on skill over college brand | Portfolio + technicals; the 20-firm boutique directory maps who to write to |

| Big 4 transaction teams → IB later | Wide entry, 1–3 year bridge | A record of deal work (Path 6 below) |

| GCCs — global banks' big India analyst hubs (Bengaluru/Mumbai/Gurugram) | Structured intakes, high volume | Campus cycles + mid-career postings; timing in the internships guide |

| Global bank front office, straight in | Narrowest — a handful of seats | Target-campus placement or an internship convert |

Pay ladder (PayScale India; checked in July 2026):

- Entry (<1 yr): ₹6.07 lakh total pay

- Average base: ₹8.86 lakh

- Top 10%: about ₹30 lakh — the widest spread of any lane here; bank tier and city decide where you land

- Source: 51 profiles, page updated 26 Mar 2026

Deal flow is real: on Tracxn's CY2025 India M&A table, Morgan Stanley led by deal value (9 deals, $16.2B) while EY (23), KPMG (20) and PwC (18) led by count.

The interview test. Walk through a model you built. Then rapid-fire technicals until something breaks — the ₹10-depreciation walk, EV bridges, why two valuations disagree. Drill the 50-question bank with model answers; clearing it without notes is your readiness gate.

Exit map (years 2–4):

- PE/VC associate — the classic next step

- Corporate development — the in-house deals team of a large company

- FP&A or strategy — the lifestyle switch; mapped in IB exit opportunities

Pick this lane if you want maximum learning per month and can trade evenings for it in your twenties. Avoid it if predictable hours are non-negotiable — no pay fixes a rhythm you hate.

Path 2 — Equity Research: Forecasts You Sign Your Name To

The work. A research team covers a set of listed companies — often 8–15 per senior analyst. You keep an earnings model for each company and update it within hours of results. Then the team publishes a note with a view — buy, sell or hold — and a target price.

Unlike IB, your output is public and dated. In three months, everyone knows if you were right. Start with what equity research is for the sell-side vs buy-side split (sell-side = brokerages selling research; buy-side = funds investing their own money).

A realistic Tuesday in results season:

- 8 am — your company reported at 7:45; a quick "flash note" must go out by 9

- 10 am — rebuild the quarter in the model; margins missed, so the year's forecast changes

- 1 pm — your senior decides the stance; you draft, they sharpen it

- 4 pm — three client calls, same question asked three ways

- 6:30 pm — start on the next company; it reports tomorrow

Off-season is calmer: model upkeep, industry checks, big first-time reports on new companies.

Entry doors, ranked:

- Brokerage (sell-side) research associate — the widest door; hires from campus and mid-career

- Fund-house (buy-side) research associate — fewer seats; usually wants a stock pitch you can defend

- Boutique research firms — small, skill-first, good learning

One file opens all three: a 2-page written stock pitch — your view, model summary, what will prove you right, what could prove you wrong — on a company you modeled yourself.

Pay ladder (PayScale India; checked in July 2026):

- Equity research associate: entry ₹4.15 lakh, average ₹5.92 lakh, top 10% near ₹10 lakh (n=41, updated 18 Apr 2026)

- The nearby "equity analyst" title: average ₹4.58 lakh, top 10% touching ₹20 lakh (n=32 — small sample; updated 14 Feb 2026)

- The growth seat: portfolio managers average ₹12.9 lakh, top 10% around ₹40 lakh (n=57, updated Nov 2025)

The interview test. "Pitch me a stock." Then they attack your target price — the multiple, the margin assumption, the growth number — in that order. Brokerages often add a timed model test (build or fix an earnings model in 60–90 minutes).

Exit map: buy-side research → portfolio management; company strategy or investor-relations teams; some move into IB for their sector.

Pick this lane if you like going deep on a few companies, writing, and being measurably right or wrong. Avoid it if you dislike writing — half this job is prose.

Path 3 — FP&A: The Company's Own Modeler

The work. FP&A (financial planning & analysis) is the company modeling itself. Three products on a loop:

- The annual budget — next year's plan, in numbers

- Rolling forecasts — the plan, refreshed as reality arrives

- Variance analysis — explaining gaps between plan and actual ("variance" just means the gap), in words a CFO can repeat to the board

Every large company runs this function. That makes FP&A the highest-volume lane by openings — and the most spread out. You are not chained to Mumbai.

A realistic Tuesday in month-end week:

- 9:30 am — last month's numbers landed in the accounting system overnight; refresh the pack

- 11 am — marketing overspent 12%; call them — is it timing, or a real overrun?

- 2 pm — re-forecast the quarter with the new spending pace

- 4 pm — the CFO wants one slide: what changed, why, what we do about it

- 6 pm — done. Non-close weeks are calmer still

Here is the daily artefact itself. Interviewers expect you to read one instantly:

Entry doors, ranked:

- GCC / shared-services FP&A hubs (Bengaluru, Hyderabad, Gurugram) — highest volume, structured intakes

- Listed-company FP&A teams — steady mid-career hiring

- Startup finance teams — broadest role, thinnest supervision; you learn fast

- Adjacent feeder: "Business Analyst, Finance/Banking" averages ₹7.97 lakh (n=187, updated 6 Apr 2026)

Pay ladder (PayScale India; checked in July 2026):

- Financial planning analyst: entry ₹5.0 lakh, average ₹8.08 lakh (n=32 — small sample; updated 19 Jan 2026)

- The broader "financial analyst" title — the biggest dataset in this post: entry ₹3.88 lakh, average ₹5.70 lakh (n=1,102, updated 25 May 2026)

- The ladder is the argument — controller: ₹19.8 lakh average, top 10% ₹40 lakh (n=313); CFO: ₹37.6 lakh average, top 10% ₹80 lakh (n=272)

The interview test. Three parts, usually:

- A variance case — "marketing is 12% over; walk me through your first hour"

- An Excel screen — often live, building a quick forecast from messy numbers

- A people scenario — deliver bad news to a department head without burning the relationship

Exit map: FP&A manager → controller → CFO track; corporate development (the internal deals team); or a sideways move into Big 4 advisory for deal exposure.

Pick this lane if you want real modeling with sane hours, inside a business you can influence. Avoid it if you need deal adrenaline — month-end close is a rhythm, not a rush.

Path 4 — Private Equity & VC: The Later Door

The work. Funds invest rather than advise. A PE associate:

- Screens companies the fund might buy

- Builds LBO models (deals done mostly with borrowed money)

- Runs due diligence — the deep pre-deal check — managing the Big 4 teams from Path 6

- Drafts the investment-committee note: the write-up asking the fund's bosses for a yes

- Then watches portfolio companies for years — the part outsiders forget

VC associates do the same motion earlier-stage: sourcing calls, market maps, and cap tables (the sheet showing who owns how much of a startup).

A realistic Tuesday (PE associate):

- 9:30 am — the due-diligence team's draft cut your deal's profit number by 8%; rework the sums

- 11 am — at the new number, the deal only works at a lower price or with more debt

- 2 pm — call with the target company's CFO; ask about the March revenue spike, politely

- 5 pm — draft the investment-committee note

- 7 pm — one portfolio company's monthly report shows a loan condition getting tight; flag it

Scale of this world: Bain & Company's India Private Equity Report 2026 (with IVCA) counts roughly $36 billion of PE-VC investment across ~1,700 deals in 2025.

Entry doors — read this honestly. The fresher door barely exists. Indian funds run tiny teams and hire people with 2+ years in IB, Big 4 deal teams or research. Treat PE as your second job:

- The reliable sequence: modeling → deal seat → fund (mapped in IB vs PE vs VC and IB exits)

- Rare direct doors: analyst programs at a few large funds; portfolio-monitoring roles that convert inward

Pay — with heavy warnings (PayScale India; checked in July 2026):

- PE associate: ₹8.10 lakh average — but only 8 profiles, on a page last updated January 2025. A tiny, stale sample

- Its mid-career figure (₹34 lakh total pay, 5–9 years) hints at the real slope — also tiny

- VC associate: ₹17.25 lakh — PayScale shows no sample count; the firmer number is its venture-capital industry page: ₹20 lakh average across roles (n=30, updated 17 May 2026)

- Honest summary: fund seats usually out-earn banking batchmates, on far fewer seats. "Carry" — a share of fund profits — arrives only at senior levels. India's public data here is too thin to promise anyone a number

The interview test. A "paper LBO" — deal maths done aloud, no Excel. A deal you would do, and why. For VC: a market map with your own sourcing angle. Funds test judgment; they assume you have the mechanics.

Pick this lane if you are patient enough for the two-step route and want to own decisions, not advise on them. Avoid it if you need the seat this year — forcing a fresher PE entry mostly produces disappointment.

Path 5 — Credit Desks: Models That Decide Loans

The work. Before a bank or NBFC (a non-bank lender) gives a company a loan, someone projects the borrower's cash flows and asks: will they repay? That someone is you. The daily outputs:

- A borrower model with stress cases ("what if sales fall 20%?")

- A credit appraisal memo — business, financials, security offered, ratios vs policy

- Monitoring notes on loans already given

Two ratios run this world. DSCR — debt-service coverage ratio — asks: does the company earn enough cash to pay its loan instalments? Leverage asks: how big is the debt versus profits?

A realistic Tuesday:

- 9:30 am — a relationship manager wants loan terms for a ₹40-crore request by Friday

- 12 pm — base case works: DSCR 1.4× clears policy. Then your rates-up stress case fails it

- 3 pm — call back with a structure that works: shorter tenure, more collateral

- 4:30 pm — quarterly review: two existing borrowers show receivables slipping; draft the early-warning note

Steadier than deal work — and constantly hiring.

Entry doors, ranked:

- NBFC credit teams — widest door; high volume, faster responsibility

- Bank credit-analyst programs — structured, process-heavy, excellent training

- Rating agencies — analytical and writing-heavy; a respected springboard

This lane also neighbours credit-risk modeling — building the statistical models (PD/LGD/EAD, ECL) behind lending — if you later add statistics and Python. That bridge is mapped in the credit-risk career guide.

Pay ladder (PayScale India; checked in July 2026):

- Credit analyst: entry ₹4.14 lakh, average ₹8.13 lakh, top 10% near ₹20 lakh (n=122, updated 27 May 2026)

- Early-career (1–4 yrs) already ₹8.21 lakh — the strongest early jump in this post's data

- The risk-side growth seat: risk managers average ₹14.3 lakh, top 10% ₹30 lakh (n=97)

The interview test. Read a balance sheet cold and say what worries you. Compute and interpret DSCR. Defend a "no" — "the promoter is well-connected; why did you decline?" Process discipline is tested as hard as analysis.

Exit map: senior credit and underwriting roles; credit-risk modeling teams (via statistics); structured finance; funds that buy troubled loans — the credit-native corner of PE.

Pick this lane if you want banking-adjacent modeling with process discipline and volume hiring. Avoid it if saying "no" politely, often, and in writing drains you — that is half the job.

Path 6 — Big 4 Transaction Advisory: Deals With Training Wheels On

The work. Due diligence, valuations and M&A support inside Deloitte, PwC, EY and KPMG — plus the strong next tier (Grant Thornton Bharat and peers). The signature product is the QoE — quality of earnings — analysis: cleaning a company's reported profit down to what is repeatable, before a buyer prices it.

Alongside the QoE sit working-capital and net-debt analyses. These move the final deal price rupee-for-rupee. You see more deals per year here than almost anywhere else — with senior review on everything.

A realistic Tuesday on a live deal check:

- 9:30 am — the data room (the deal's shared document vault) opened three new folders overnight; split them with your senior

- 11:30 am — March revenue looks pulled forward; trace invoices to April credit notes, draft the finding carefully

- 2 pm — management Q&A call: twelve questions asked, four answered, eight "will revert"

- 5 pm — update the databook; the profit bridge now carries six adjustments

- 7:30 pm — partner review: two findings survive, one needs more evidence

Deal-season weeks run long. Between deals, you breathe.

Entry doors:

- Structured campus intakes, plus year-round mid-career postings for analysts with demonstrated modeling

- Internal transfers from audit — common for CAs; the CA-specific route is in FM for CA students

- Proof the doors are real: all four Big 4 networks' India entities appear on ICAI's 63rd campus-recruitment list (Dec 2025–Jan 2026; ICAI 64th-round brochure, checked in July 2026)

- Proof the work exists: EY (23), KPMG (20) and PwC (18) led Tracxn's CY2025 India M&A count table

Pay ladder — honest brackets. No PayScale India page isolates "transaction services analyst", so:

- Junior end tracks the financial-analyst band: entry ₹3.88 lakh (n=1,102)

- The skill premium shows later: PayScale's "Mergers and Acquisitions" skill page averages ₹20 lakh across all job titles reporting that skill (n=73, updated 24 May 2026) — a mixed junior-to-director figure, not an entry salary

- Realistic read: advisory starts below front-office IB and compounds through the manager ladder or a deal-side switch

The interview test. An EBITDA-adjustment case ("the owner pays himself ₹5 crore above market — what happens to the price at 8× EV/EBITDA?"). A working-capital discussion. An Excel databook exercise. CAs get deeper accounting probes; non-CAs get "can you read messy statements" probes.

Exit map (years 2–4): IB — the classic switch, your deal record is the bridge; PE deal or operations teams; corporate development; or the internal partner track.

Pick this lane if you want deal exposure with mentorship, reps and a brand-name springboard. Avoid it if you want to run the deal rather than check it — advisory supports decisions; it does not make them.

Who Actually Hires Modelers in India?

Names beat adjectives. Two windows you can verify yourself:

Window 1 — ICAI's campus recruiter list. The 63rd campus round (Dec 2025–Jan 2026) drew 145 organisations (ICAI 64th-round brochure, checked in July 2026). The list reads like this post's six lanes wearing name tags:

- Advisory lanes: all four Big 4 networks' India entities, Grant Thornton Bharat, MSKA & Associates

- Markets & quant hubs: Nomura Services India, D.E. Shaw India, BSE, NSE

- Credit desks: DBS Bank, ICICI Bank, Axis Bank, IDFC FIRST Bank, Bajaj Finserv, EXIM Bank, SIDBI

- Corporate FP&A at scale: Reliance Industries

These firms recruited CAs in that round — and every one of them also runs analyst teams that hire modeling-skilled graduates through the year.

Window 2 — deal-market league tables. Tracxn's CY2025 India M&A table shows Morgan Stanley leading by value (9 deals, $16.2B), with EY, KPMG, PwC and Kotak leading by count. On the investing side, Bain-IVCA counts ~$36B across ~1,700 deals in 2025. Every one of those transactions consumed models — pitch, diligence, LBO, credit.

City reality:

- Mumbai — front-office IB and sell-side research concentrate here (BKC, Lower Parel), some in Gurugram

- Bengaluru / Hyderabad / Gurugram — the GCC hubs; the volume door outside Mumbai

- Everywhere — FP&A and credit; every company budgets, every lender underwrites

Plain takeaway: the demand side is not hypothetical — it is a recruiter list you can read and league tables you can count. Pick a lane whose employers exist in your city, or plan the move.

The Six Lanes, Side by Side

One-sentence read: entry averages cluster within a few lakh, so choose by trajectory and temperament — the divergence comes later, and fastest in deal-side lanes.

| Lane | Typical hours | Entry difficulty | Five-year trajectory |

|---|---|---|---|

| Investment banking | Longest; deadline-driven | High — few seats, portfolio + technicals screened hard | Associate → VP, or exit to PE/corp dev |

| Equity research | Long around results seasons | Medium-high — writing sample + model test | Senior analyst with a named coverage list; buy-side moves |

| FP&A | Predictable; month-end peaks | Medium — most openings of any lane | FP&A manager → controller track |

| PE / VC | Deal-driven bursts | Very high directly; normal via IB/Big 4 first | Associate → principal, carry begins |

| Credit desks | Steady; process-bound | Medium — strong hiring volume at banks/NBFCs | Senior credit roles, or pivot to risk modeling |

| Big 4 advisory | Long in deal season | Medium — structured intakes + laterals | Manager, or springboard to IB/PE |

Plain takeaway: IB pays fastest and costs the most hours; FP&A and credit offer the most seats and the most sleep; PE is a second job, not a first one.

Switching Lanes Later: What It Costs

Your first lane is not a life sentence. The model skills transfer intact, and some switches are so common they have worn paths:

| The switch | Typical window | The bridge you must carry | Difficulty |

|---|---|---|---|

| Big 4 advisory → IB | Years 1–3 | A deal-sheet: named (or anonymised) diligence/valuation work you can walk through | Moderate — the classic switch |

| IB / Big 4 → PE | Years 2–4 | Live-deal record + paper-LBO fluency; funds interview judgment | Hard — few seats, timing matters |

| Credit analysis → credit-risk modeling | Years 1–3 | Statistics + Python or SAS on top of your lending sense — see Python vs SAS | Moderate — hot demand through the ECL transition |

| FP&A → corporate development | Years 2–4 | Valuation practice beyond budgeting — an M&A model or two in your portfolio | Moderate — internal moves are the cheat code |

| Sell-side research → buy-side | Years 2–5 | A public (or demonstrable) record of calls that aged well | Hard — seats are scarce and picky |

| IB → FP&A / strategy | Any time | Nothing new — the lifestyle downshift is always open | Easy |

Plain takeaway: pick your first lane knowing the second usually stays reachable. Only PE and buy-side research punish waiting — if either is the dream, sit in a deal-facing lane first, not a comfortable one.

Which Path Fits You?

Four questions settle most cases:

- Deal adrenaline or operating rhythm? Adrenaline → IB or Big 4 advisory. Rhythm → FP&A or credit.

- Advise, invest, or run? Advise → IB/advisory. Invest → research now, PE later. Run → FP&A — the road to controller and CFO seats.

- Writer or builder? Research rewards people who can argue a view in print. Pure builders thrive in IB and FP&A.

- How soon do you need the job? FP&A and credit hire in volume year-round; IB and research hire in narrow windows. Short runway → take the volume lane, switch later. The table above shows the paths stay open.

Torn between a skill course and a credential instead? That sequencing question is answered honestly in FM vs CFA. CA-background readers have a dedicated map in FM for CA students.

The 90-Day Break-In Plan

Whatever lane you choose, the entry mechanics are identical: portfolio → applications → interview reps. Ninety days, three gates:

| Phase | Do | Gate before moving on |

|---|---|---|

| Days 1–45 — Build | Complete the ladder on one real company: 3-statement → DCF → comps (add an LBO only for IB/PE aims) | Balance sheet balances every year; you can defend each assumption in two sentences |

| Days 46–60 — Package | One-page CV around the portfolio (the resume guide + free resume evaluator); LinkedIn headline that names the skill, not the dream | Evaluator score 85+; two seniors have torn the model apart and you fixed what they found |

| Days 61–90 — Apply + drill | 15 tailored applications/week across your lane + one adjacent lane; nightly reps on FM interview questions (add IB technicals for deal-side) | 3 interviews reached; every model question in your last mock answered without notes |

Add one lane-specific proof to the portfolio:

- IB — a one-page pitch summary

- Research — a 2-page written stock view

- FP&A — a variance pack (like the figure above) on your modeled company

- Credit — a one-page loan memo with DSCR and a stress case

- Big 4 — an EBITDA bridge with three defended adjustments

- PE aim — do the IB proof, plus a paper-LBO walkthrough

Fall-behind rule: if the build phase overruns, cut scope (drop the LBO) — never quality. A balanced small model beats an impressive broken one in every interview that matters.

Financial Modeling Career Paths: Frequently Asked Questions

At entry, investment banking leads on PayScale India — ₹8.86 lakh average, top 10% near ₹30 lakh (n=51). Across lanes, though, entry averages cluster between ₹5.7 and ₹8.9 lakh. The real gaps open after year three: deal roles and fund seats pull away, and FP&A's ladder reaches controller (₹19.8L avg) and CFO (₹37.6L avg). PE likely out-earns them all — on samples too small to quote responsibly.

Rarely — do not plan on it. Indian PE funds run small teams and hire people with two-plus years in investment banking, Big 4 deal teams or research. The reliable route is: modeling course → deal-side seat → fund. Treat any course promising direct PE placement with scepticism.

No — it is a different trade, not a lower one. FP&A offers more openings, humane hours, and a direct ladder to controller and CFO roles — seats averaging ₹19.8 lakh and ₹37.6 lakh on PayScale India's two largest samples here (n=313, n=272). IB offers faster learning and pay, at a steep lifestyle cost. The lanes converge at the top more than fresher forums admit.

Not to start — the portfolio gets you the first seat. Credentials compound later: CFA strengthens research and buy-side moves; CA strengthens advisory and CFO-track credibility. The sequencing logic is in FM vs CFA: skills first when you need employment soon; credential first only when you are sure of the destination and funded for the wait.

The lanes that screen on skill rather than degree brand: FP&A at the big GCC hubs, credit desks, and boutique IB — all three interview on the portfolio itself. Engineers also get pulled toward credit-risk modeling and quant seats, where their math transfers directly — see FRM for engineers. The statement-reading gap closes in weeks of practice; the model files matter more than your major.

Honestly: AI is compressing the mechanical parts of all six — deck formatting, first-draft comps, data pulls. It is raising the value of judgment: which assumption is wrong, which lender blinks, which forecast the CFO will own. Lanes built on client trust and accountability — advisory, FP&A partnering, credit committees — automate slowest. Full analysis: will AI replace finance jobs?

Adjacent switches — Big 4 advisory to IB, credit analysis to credit-risk modeling, FP&A to corporate development — typically happen inside 1–3 years, because the model skills transfer intact. You are re-proving context, not capability. The hard jumps are into PE (needs a deal-seat record) and buy-side research (needs calls that aged well). The full cost of each switch is in the table above.

Only two concentrate there: front-office IB and sell-side research live largely in Mumbai. Global banks run large analyst hubs (GCCs) in Bengaluru, Hyderabad and Gurugram. FP&A exists wherever companies do, and credit desks hire in every banking city. If you cannot relocate: FP&A, credit and GCC roles are your realistic first seats, with a Mumbai move as a later switch if the deal lanes call.